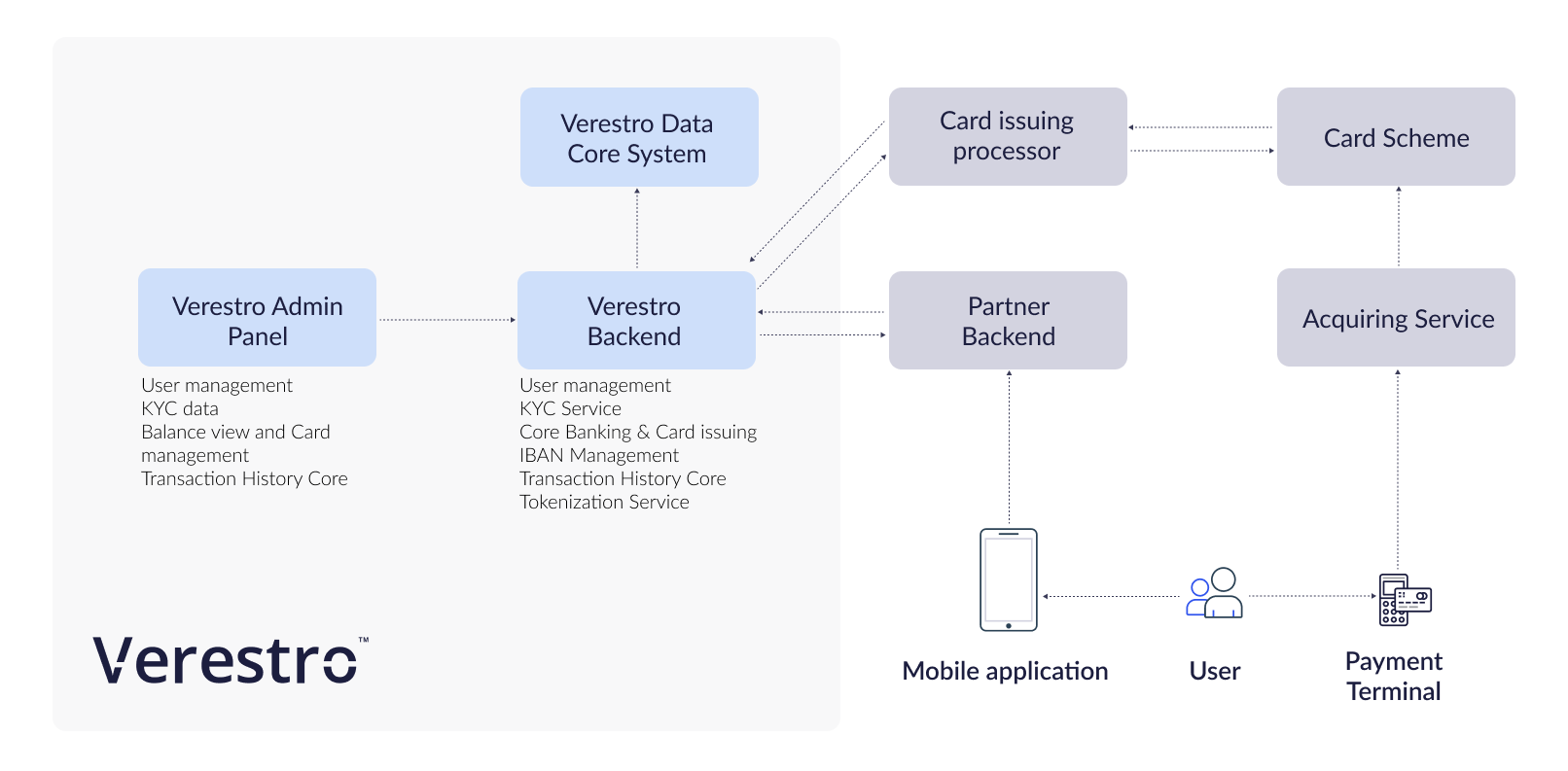

Card Issuing and Core Banking

Verestro Antaca is responsible for card issuing and account opening. The system can perform KYC and eKYC of the user before card issuing. You can manage card and user balance through Antaca.

- Article

- Payment schemes

- Ranking of card issuing companies

- Regulatory and license impact on card issuing

- PCI DSS & other security requirements

- Multicurrency cards - 3 implementation options

- How to prepare for a card issuing project?

- Card Lifecycle Management

- VISA or Mastercard?

- Prepaid, debit or credit cards - the main differences

- Tips to avoid problems when implementing card issuing

- BIN Range or Separate BIN in Card Issuing

- IBANs, cards, balances - how to manage all of this?

- Issuing cards in various currencies

- What steps should be taken to start a card issuing project with Verestro outside the European Economic Area?

- What are the legal and payment scheme rules for launching a prepaid card program without KYC?

- Card Program – in-house or via BaaS?

- Reverse solicitation – marketing & promotion of card issuing in multiple countries

- Introduction

- Intro slides

- Overview

- Quick start

- Transactions Flow

- Technical documentation

- Your APIs for us - External Balance

- Your APIs for us - Shared authorization

- Your APIs for us - Notifications

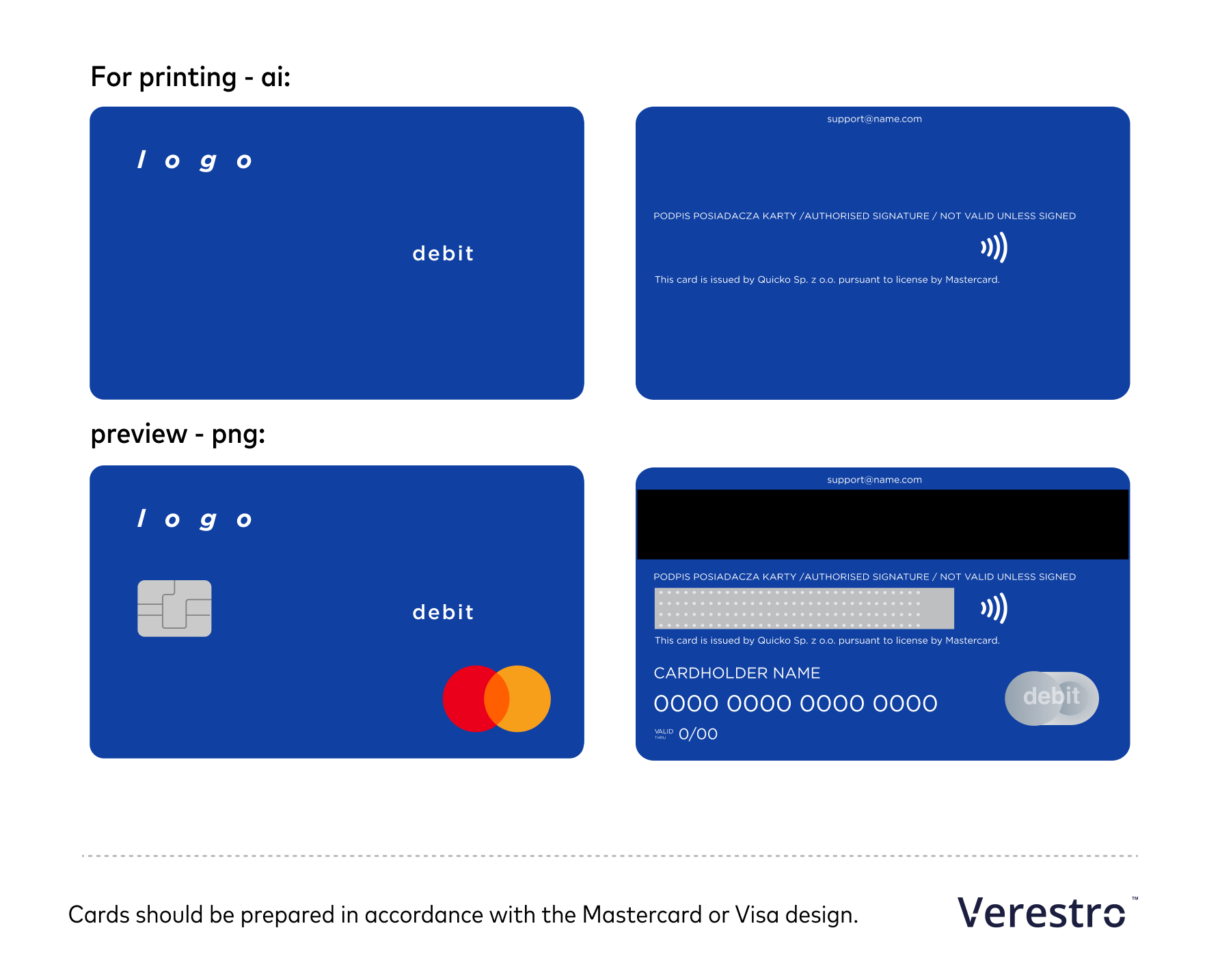

- Digital Cards Design

- Physical Cards Design

- Legacy Transactions Notifier

- Frequently Asked Questions

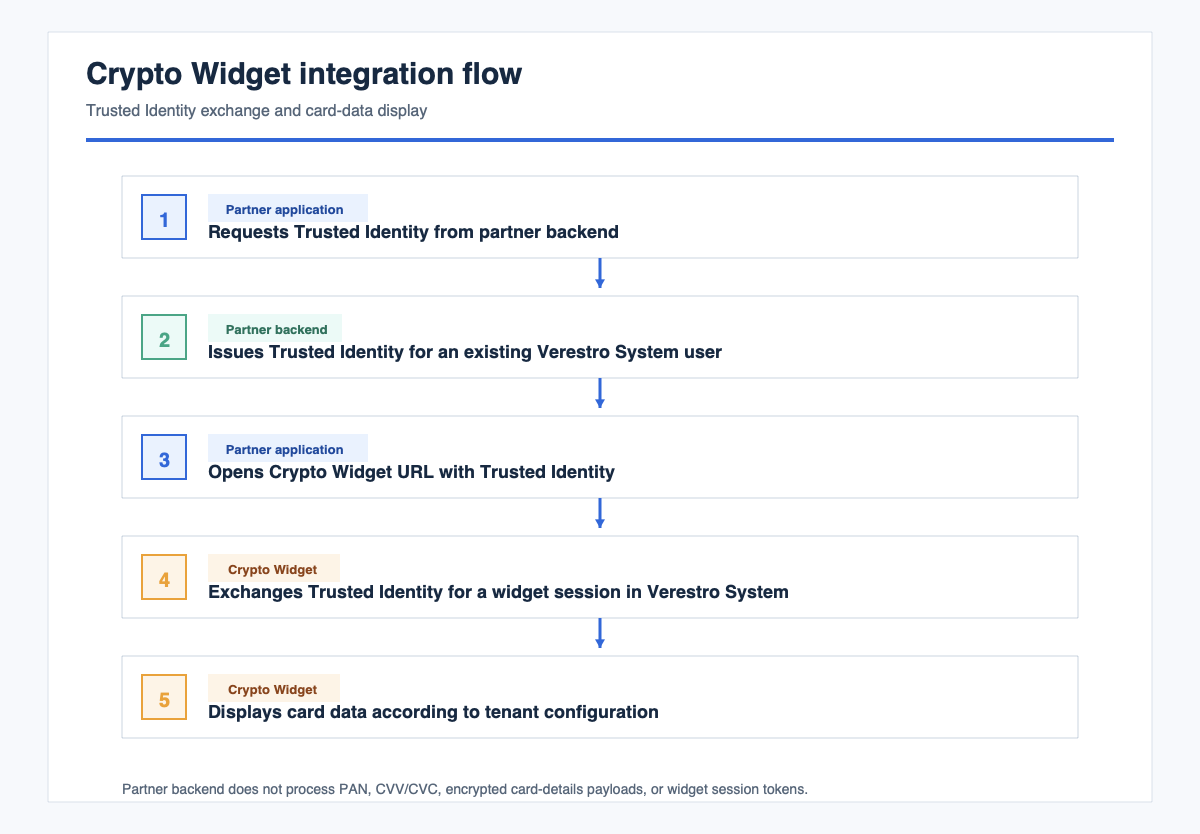

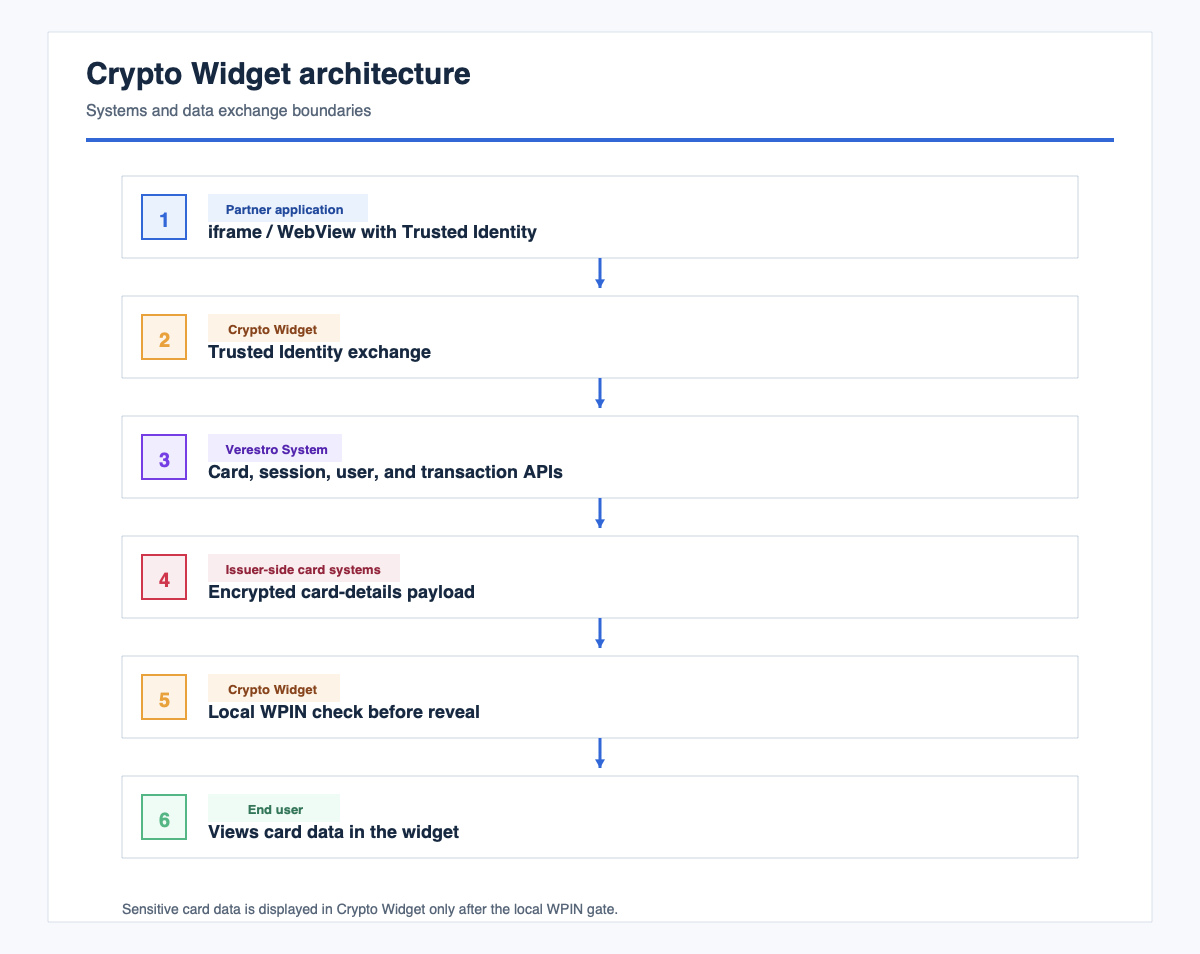

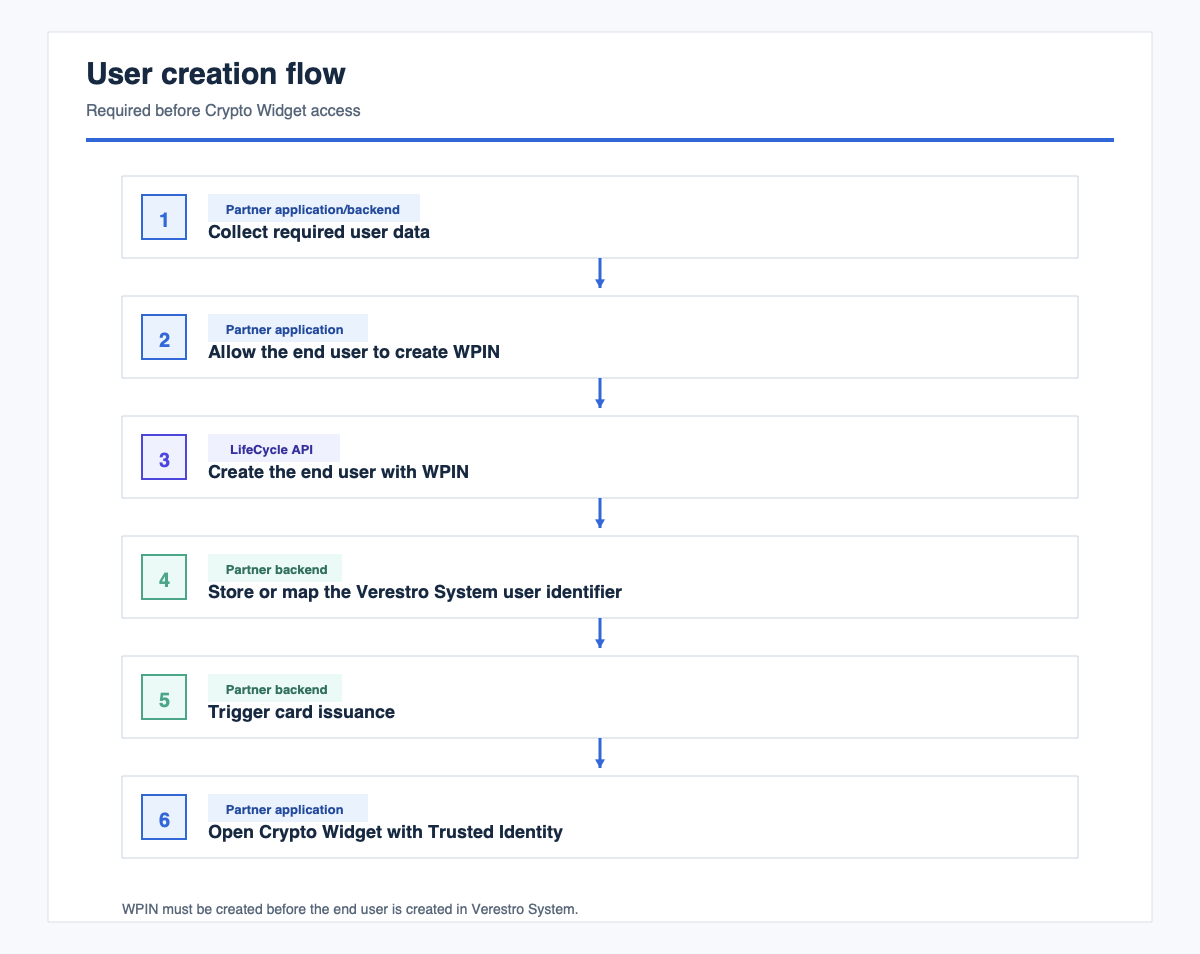

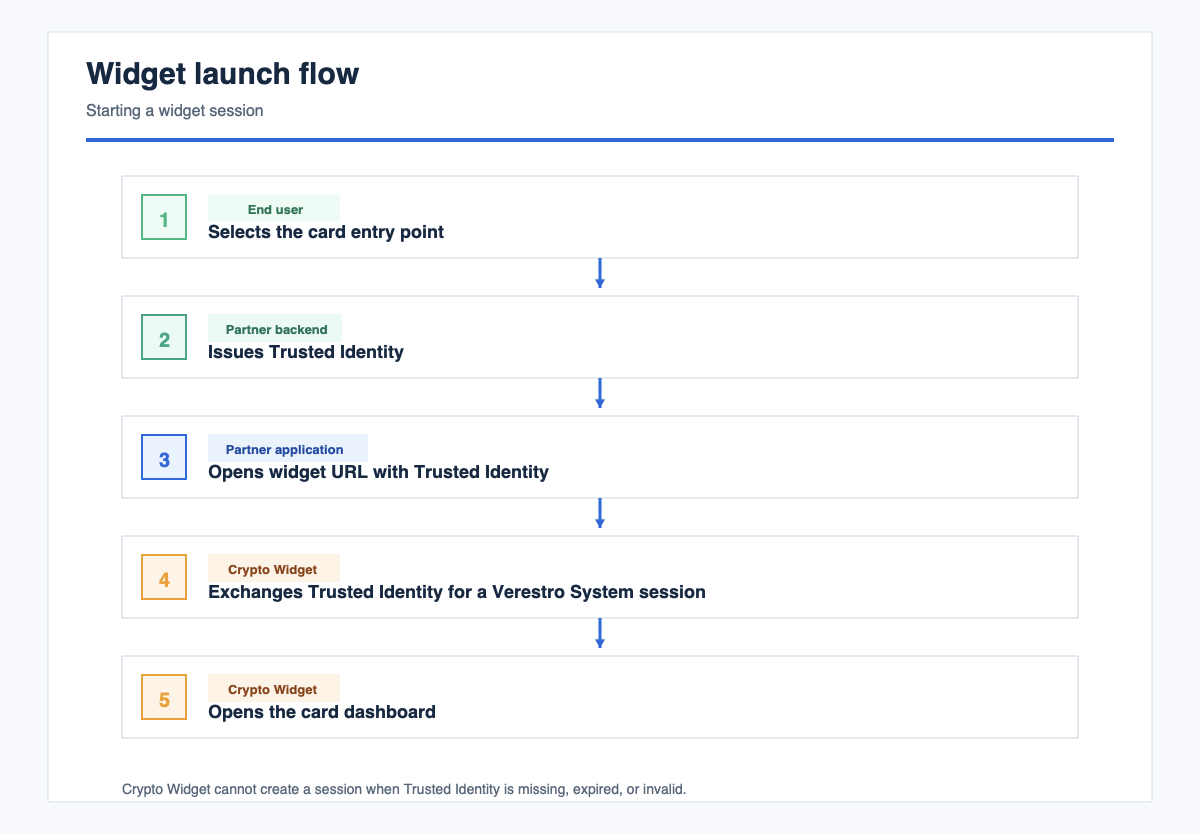

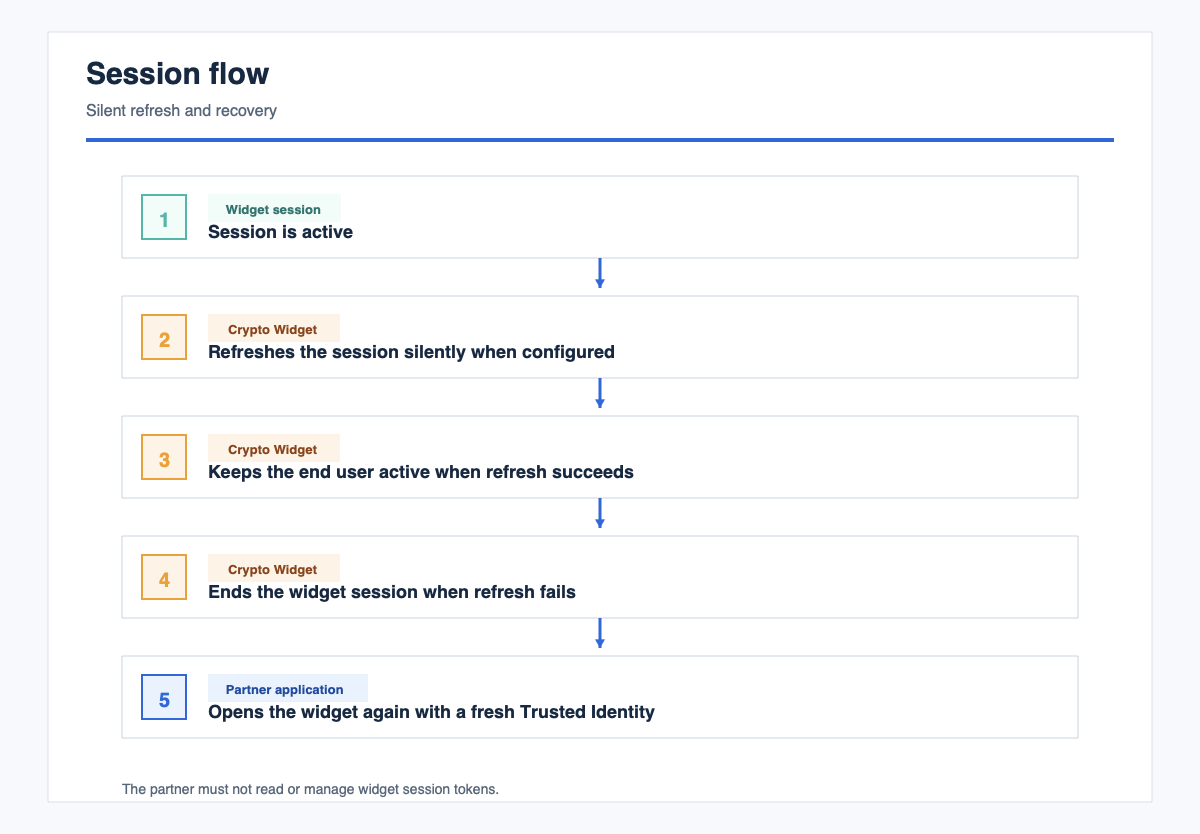

- Crypto Widget - webview/iframe for your application

Article

You can find more knowledge about products on this site.

Payment schemes

In this document we describe how payment schemes (Mastercard and VISA) work.

Payment card business is a large global market, which was developed in the USA in the first half of XX century and has grown globally. In this document we will describe the main business principles and in the next chapters we will go into more details. We will focus mainly on Mastercard and VISA operations, as these are the largest payment schemes in the world and the main partners we work with.

Four Party Model

Let's start with the general relationships between the parties. In the Mastercard and VISA 4-party model (which is actually 5-party model) there are the following players:

1. Cardholder - has a contract with Card Issuer, which is usually a bank, financial institution, payment institution, credit union, etc. Cardholder keeps a card in a plastic or virtual form that he/she gets from Issuer. Cardholder makes a purchase transaction at Merchant or sometimes withdraws money from an ATM. In the case of an ATM transaction, the ATM operator (usually a bank) acts as Merchant in a standard purchase transaction.

- Cardholder is happy because he/she does not need to carry cash all the time and has money all the time in their pocket or phone.

- Cardholder has to pay card fees to Issuer for getting a payment card.

2. Merchant - delivers goods to Cardholder, but does not receive cash immediately, but accepts the card transaction, which gives him/her almost 100% confidence that he/she will receive money in a few hours or days.

- Merchant is happy because he/she sold goods, usually having sold more than Cardholder could afford with cash. Imagine the situation where you have to pay cash all the time. Would you always carry enough cash with you? What if you want to buy something, but you do not have enough cash?

- Merchant has to pay the so called "Merchant Fees" to Acquirer for processing the transaction. Usually, Merchant Fees are between 0,5-3% depending on transaction value, country, merchant segment, type of card etc. Merchant fees cover most, if not all, of the transaction processing costs. They usually include all the fees charged by Acquirer, Issuer, Mastercard or VISA for the transaction.

3. Issuer - Issuer is usually a bank, credit union or any other payment institution that delivers payment cards to cardholders (consumers or businesses). Issuer signs contracts with cardholders. On the other side of business, Issuer has a franchising or licensing contract with VISA and Mastercard and connects to their network using Issuing Processors. Verestro and our partners plays the role of Issuer and Issuer Processor in our card issuing or BIN sponsorship projects. During the transaction process, Issuer usually gets authorization, clearing and settlement messages that result in transfer of money from a cardholder account to Acquirer so that Acquirer could settle the transaction with Merchant.

- Issuer is happy because they charge card fees to Cardholder (for example monthly per card) and get transaction fees called Interchange Fee from Acquirer. Interchange fee is a very important part of Merchant Fees. In the European Union for consumer cards it is usually in the value of 0,2-0,3%, but in many countries, especially for business and credit cards, it can amount to 1-2% of the transaction value.

- Issuer has to cover costs of card issuing, which include:

- Cost of payment scheme (Mastercard or VISA) incl. monthly connection, license, authorization, clearing and many many other fees. This is usually the main part of Issuer's costs.

- Cost of other processors incl. transaction authorisation, card maintenance, card tokenization, plastic card manufacturing, personalisation, delivery, etc.

- Regulatory costs incl. payment license operations, Anti-Money Laundering processes, etc.

- Various costs connected with maintaining a relationship with Cardholder incl. proper communications, SLAs, etc.

4. Acquirer - Acquirer is usually a bank or payment institution that signs contracts with merchants, settles payment transactions with merchants and has acquiring contracts with a payment scheme. Acquirer usually provides a payment terminal to merchant locations, and makes sure if it works and is ready for transactions.

- Acquirer is happy because they charge Merchant Fees that usually consist of transaction fees (0,5-3%), sometimes fixed fees per transaction (0,01-0,5 EUR) and monthly fees per terminal.

- Acquirer needs to cover various fees, including regulatory fees, payment scheme costs, cost of processors, terminal purchase and costs of operations.

5. Payment Scheme - Payment Scheme (i.e. Mastercard or VISA) are key for keeping the model running. They develop technical systems that issuers and acquirers are connected to, they process transactions, they develop the market. However, they are also the biggest beneficiaries of the market growth as every new transaction represents revenue for Mastercard and VISA.

Key Processes

There are several processes that take place during card and transaction processing, and here we will briefly describe the most important ones:

- Card issuing process - this process or set of processes consists of multiple actions that Card Issuer needs to perform to issue a payment card. They are the following:

- regulatory compliance - every card issuer in the world needs to comply with law, get license from a national bank or financial regulator, work according to their recommendations and rules,

- Mastercard integration and licensing - it consists of a formal process, providing necessary cash collaterals, doing technical integration, getting security certifications etc.,

- card creation process - after signing a contract by a user, Card Issuer needs to create a new card number (using BIN of the issuer - BIN = first 6 or 8 digits of card). When a card number (PAN = Primary Account Number) is created, the card can immediately work as a virtual card or can be sent for personalisation if it is a plastic card. Usually, after the user receives the card (virtual or plastic), the user starts the card activation process, sets the card PIN and can start using it.

- Transaction process - this process consists of several operations that result in transfer of money from Cardholder account to Merchant. They are the following:

- Authorization process is an action that ensures that Merchant can immediately get information if Cardholder has money on his/her card account and if this card is not stolen. The authorisation can happen online (a direct request to Issuer's system to check the balance and card status) or offline (in this case a chip on the card makes a decision if it can approve the transaction without asking Issuer's systems).

- Clearing process is an action of payment scheme during which clearing files are delivered by acquirers to payment scheme and payment scheme calculates how much money each Acquirer should receive from each Issuer in the world.

- Settlement process is a process of transferring money from issuers to acquirers and later to merchants so that finally Merchant receives the transaction amount, less Merchant Fees, on his/her bank account. Every Issuer and Acquirer has settlement bank accounts that are used for transferring money from or to. Payment Schemes operate those accounts using something like Direct Debit / Credit to transfer money between Settlement Accounts of various financial institutions.

- 3DS - sometimes additional authentication mechanisms are used to ensure that the person initiating the card transaction is the actual cardholder. In the case of eCommerce transactions this process is called 3DS. During an Internet transaction, the user's browser opens the bank's website, where the user can authenticate the transaction using one-time passwords or other forms of authentication developed by Issuer. After the 3DS authentication is verified, Acquirer receives a special cryptogram that is included in the authorization message and validated later by Issuer during the authorization process.

- Tokenization - tokenization is a process of exchanging a real card number into a token number (similar to a card number) to enable digital and contactless payments. Usually it is connected with transactions performed in cooperation with the so called X-Pays (i.e. Apple Pay, Google Pay, Fitbit Pay etc.). The process of tokenization requires an integration with Mastercard Digital Enablement System (MDES) or Visa Tokenization system (VTS) to enable tokenized payments.

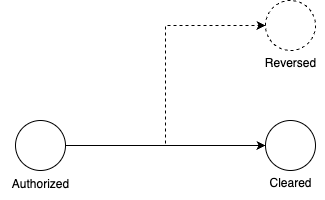

- Refund and reversal - special type of transactions that enable reversing payment transaction either immediately (reversal) or later (refund). Once this process has been initiated, Cardholder can receive money back after successful authorisation.

- Chargeback - process of complaint management. It can be initiated by Issuer in case Cardholder informs Issuer that he/she did not do the transaction or did not authorize it, or goods were not delivered etc. The process is costly for Issuer and Acquirer but ensures security of the system for cardholders.

- Card-to-card transactions and payouts - the so called "payment" or "credit transactions". In a standard purchase transaction money is transferred from Cardholder to Merchant. In a card-to-card transaction or payout transactions, the user gets money on his/her card or on the account linked to the card.

There are other important processes associated with payment systems and card transaction processing, but let's stop here and take a short break to understand these critical processes.

Ranking of card issuing companies

How to choose a BIN sponsor and card issuing partner?

Choosing a BIN sponsor or card issuer is a difficult decision for many partners. Most of our partners do not come from the payment card business, so they learn by doing. In this chapter, we are going to describe the key decision factors of choosing a card issuer and make a simple ranking that we will be upgrading and updating in the coming months and years, as not all information is available to us immediately. On purpose, we will not compare other companies to us, it would not be fair to include Verestro - our goal is to educate in this article.

There are the following key decision factors in choosing a card issuing partner:

-

- Does the card issuer share 100% of interchange with me?

- What is the currency conversion rate that the card issuer shares with me?

- How can I impact and earn on ATM withdrawal fees?

- How can I impact and earn on various consumer fees?

- Can the partner help me with getting the Mastercard or VISA marketing and financial support in the short and long run?

2. COSTS - Obvious point.

-

- What are fixed and variable fees?

- What is the level of fees in case of low volumes and high volumes?

- Is there any opportunity to minimize costs as the business grows?

- Read this article for more info on standard card issuing costs: Card issuing - financial details

3. FUNCTIONALITY & SERVICE - a very important point. Critical in the long run.

-

- Does the partner have mandatory functionalities?

- Does the partner offer currencies that I need for my users?

- What are other products that can increase usability or profit that the partner offers?

- Maybe a loyalty program?

- Any insurance offers and additional benefits that could be sold to customers?

- Perhaps invoice scanning and expense management?

- Maybe white label solutions?

- Card reload mechanisms?

- Payouts to cards?

- etc.

- Does the partner offer quick access to a developer zone or a test environment?

- Does the partner make their APIs public?

3. SECURITY AND FINANCIAL STABILITY - a critical point. Maybe it should be the first one.

-

- Is the partner a small start-up, burning money or a payment institution generating profits? Can you imagine what would happen to your portfolio and users in case of bankruptcy or hostile takeover?

- Who are the shareholders of the partner? Are these venture funds or strategic, long term investors?

- Does the card issuer make their financial statements public?

- Does the partner offer support in solving PCI DSS issues (Payment Card Industry Data Security Standards)?

- Is the partner audited annually?

- Does the partner work with banks and other large financial institutions or focus only on small, high-risk startups?

- Is the partner a small start-up, burning money or a payment institution generating profits? Can you imagine what would happen to your portfolio and users in case of bankruptcy or hostile takeover?

Here's an initial comparison of the best known card issuers in the European Union (grades: low - high):

| Name | Country | Revenue Share | Costs | Functionality & Service | Security & Financial Stability |

| Treezor.com | France | Medium | High | Medium | Medium |

| Swan.io | Denmark | Medium | High | Medium | Medium |

| Dipocket.org | Lithuania | High | Medium | Low | Low |

| Solarisgroup.com | Germany | Medium | High | Medium | Medium |

| Wallester.com | Estonia | Medium | Medium | High | Medium |

| Stripe | USA | Low | High | High | High |

| Weavr.io | Malta | Medium | Medium | Low | Medium |

| Verestro | Poland | Make your own assessment | Make your own assessment | Make your own assessment | Make your own assessment |

Source: Financial Stability results based on 2022 or 2023 results available in Internet; all other data from publicly available sources. Please make your own assessment.

Regulatory and license impact on card issuing

Legal issues related to regulatory or payment scheme rules often arise in questions we receive from our partners and clients. In this article I would like to summarize key dependencies, limitations and rules that have a very important impact on payment accounts opening, card issuing and also acquiring or money transfer activities.

When you are launching a payment institution, you have several areas to cover. One of the most important of them is a legal and rules area. Usually this impact can be divided into three main groups of activities: legal requirements, anti-money laundering requirements (which is a specific type of legal requirements) and payment scheme rules. Let me deep dive into each of them.

Legal requirements

To operate payment activities, almost in any country you need to get a payment license. There are various types of payment licenses depending on the country, so here I would like to summarize the most important details. In many cases you can hear about EMI (Electronic Money Institution license), Bank (Banking license), Credit Institution, Acquiring Institution etc. These requirements are usually connected with operational activities that the company needs to fulfill to perform payment operations for other entities. They consist of:

- Regulatory requirements in the areas of security, Know Your Customer, AML, liquidity operations, organizational structure etc.

- Audits performed by regulator

- Risk of penalties for both the company and sometimes persons involved in payment companies

- Outsourcing activities compliance

- Local laws that forbid processing customer or transaction data outside of the country

- etc.

It is important to understand details of such requirements and to follow changes of law and rules on a regular basis.

From the business point of view those requirements force us to :

- Officially register contracts with various partners at the regulator

- Get an approval for particular actions outsourced to partners

- Perform regular monitoring of payment activities done with cards issued for users of our partners

- Follow the national and EU sanction lists

- Being ready to block any transaction, account or card at any time

For our partners - just make sure that you follow the rules we inform you about. They are critical for our activity, licenses, so in fact they are securing your business.

AML and KYC requirements

AML (Anti-Money Laundering) and KYC (Know Your Customers) are part of legal requirements but it is worth presenting them as a separate group because they usually have the biggest impact on operations. The main goal of these rules is to ensure that payment organizations are not used to launder money, support terrorist or illegal activities. They also allow governments to monitor a payment activity area which may be helpful in fighting crime activities.

Key areas of impact of those requirements can be summarized as follows:

- Payment institution is obliged to perform KYC requirements as defined by the regulator - usually consisting of collected proofs of user identity verification (documents, videos, selfie, talks, and other measures)

- In case of business customers and business accounts, not only Board Members but also Beneficiaries of the companies need to go through a KYC and sanction list screening. Beneficiary is defined usually as a person with above 25% shares

- At any moment a payment institution must be ready to present these documents to the regulator

- Persons and entities placed on sanction lists cannot use services of a payment company

- Active monitoring of payment transactions for all users is required

- Sometimes proofs of income can be required

It is interesting that AML and KYC requirements do not block us from issuing cards or opening payment accounts for partners located outside the European Union with our payment companies licensed in the European Union. We are allowed to perform payment activities for Brazil, US, China citizens, as well as the Polish, German or French ones.

Make sure that you collect user documents and provide them during the user registration to us to fulfill those requirements.

Payment Scheme requirements

Payment Schemes (Mastercard, VISA or others) have separate requirements that must be followed by their partners and licensees. These requirements are similar to the previous ones but not always the same. Key requirements that do have impact on business are:

- We are licensed for a particular country or region. In our case it is the European Union countries (in fact the European Economic Area, which is a slightly different area). It means that with our European licenses we can issue cards for people residing, having addresses or working in the European Union. In case we would like to issue cards for people or entities from outside the European Union we have to get special Mastercard approval which is not impossible but may be difficult to achieve.

- We must follow payment scheme requirements on sanction lists and scan users and beneficiaries against OFAC (US Office of Foreign Assets Control) and United Nations sanction lists.

- We must be ready to follow Mastercard technical and rules requirements that sometimes may have impact on technical setup and use cases of your users.

- In case of mandates we need to be ready to implement on time necessary system updates to reach compliance with the Mastercard network.

Problematic areas

Usually problems in a business discussion come in the following areas:

- Can we issue cards for non-EU citizens? Answer: generally yes, but sometimes there may be problems, the majority of your business must be in Europe, your user addresses or office should be in Europe etc.

- What documents do we need to transfer to you during registration? Answer: selfie, international passport is usually a minimum.

Following regulatory, AML and payment scheme rules is critical for payment companies. We do not have a choice. This is part of the game of card issuing and we must follow requirements. However, it is good that such rules exist. They make our customers' money safer and minimize much bigger risks of running or supporting illegal activities.

Thanks for reading.

PCI DSS & other security requirements

Very often customers ask questions connected with security. In this article we would like to summarize key requirements connected with Payment Card Industry Data Security Standards (PCI DSS). There are other rules that we and our partners need to follow (like GDPR for example) but it will be the topic for another article.

The most important question that needs to be answered before going into details of PCI DSS requirements is - Am I actually processing payment card data?

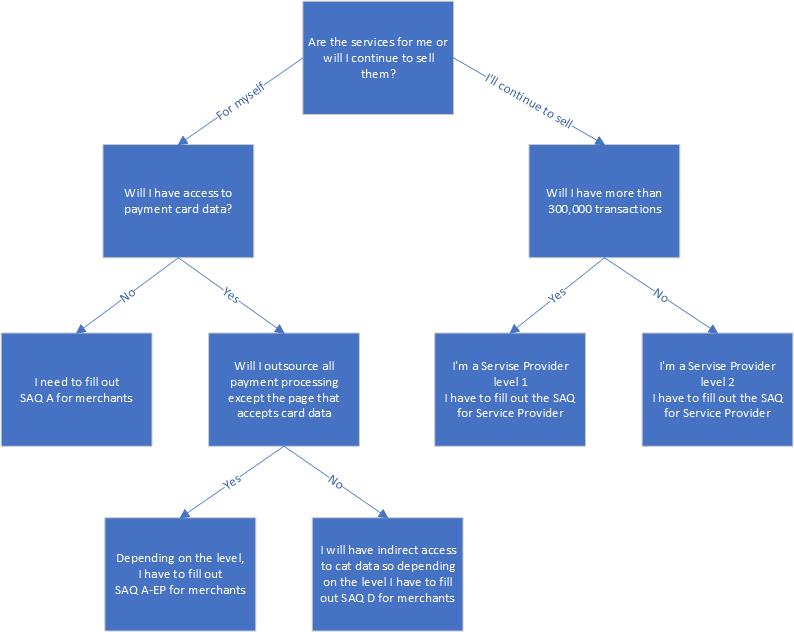

Key PCI DSS requirements mentioned below apply only in case that the partner has access to card number (PAN - Primary Account Number), expiry data or other related card data. If the partner does not touch them, if the partner cannot see those numbers there is only one requirement - a simple Self Assessment Questionnaire (SAQ) needs to be fulfilled to confirm that the partner is compliant with PCI DSS requirements.

It is very important that you choose the correct way of integration with the card issuing platform. If you use our mobile SDKs or white label products, usually you will not have access to card data and will be able to approve your project just after fulfilling SAQ mentioned above. So please consider this way of integration to avoid additional costs and risks of PCI DSS compliance. However, if you connect via API, which is a usual way of integration, you will have to comply with security rules. Please read this section twice. This is the most important - choice of integration method will be decisive if you have to or not go through annual external audits and all hassle connected with PCI DSS.

Assuming you do process card data, depending on what your role is, different levels will be applied to you. You can be a merchant or a service provider. In simple terms, if you do the work for yourself then you are a merchant if you want to further provide the service (intermediary) you are most likely a service provider. In card issuing projects you will rather be a service provider because you offer cards to your users. Let me give some examples:

Service Provider - wallet, crypto wallet, money transfer organisation offering cards to own users etc.

Merchant - an insurance company that wants to use a card to send money to their users, a lending company that wants to send a card to users, a corporation or SME giving business payment cards to their employees etc.

Who is according to PCI DSS "Merchant"

PCI DSS, or the Payment Card Industry Data Security Standard, defines a merchant as any entity that accepts payment cards (such as credit cards and debit cards) as a form of payment. The term "merchant" can encompass a wide range of businesses and organizations, including traditional retail stores, e-commerce websites, restaurants, hotels, and service providers that handle cardholder data.

Under PCI DSS, merchants are required to comply with a set of security standards and practices to protect the payment card data they handle. These security measures are designed to ensure the confidentiality and integrity of cardholder data, reduce the risk of data breaches, and protect both customers and the payment card industry as a whole.

PCI DSS compliance requirements can vary depending on the merchant's size and the volume of card transactions they process. Merchants are typically categorized into different levels based on their transaction volume, with higher-volume merchants facing more stringent compliance requirements.

There are 4 levels of compliance and requirements depending on volumes of cards and transactions.

|

Level of PCI DSS |

Your business does |

What you should do |

|

4 |

· Less than 20 000 eCommerce transactions per year · Less than 1 million other transactions per year |

· Complete an annual Self-Assessment Questionnaire (SAQ) · Conduct quarterly network scans by an Approved Scanning Vendor (ASV) |

|

3 |

· 20 000 – 1 million transactions per year |

· Complete an annual Self-Assessment Questionnaire (SAQ) · Conduct quarterly network scans by an Approved Scanning Vendor (ASV) |

|

2 |

· 1-6 million transactions per year |

· Complete an annual Self-Assessment Questionnaire (SAQ) or ROC conducted by a QSA · Conduct quarterly network scans by an Approved Scanning Vendor (ASV) |

|

1 |

· 6 million + transactions per year |

· Complete an annual internal audit · Conduct quarterly network scans by an Approved Scanning Vendor (ASV) |

Who is according to PCI DSS "Service Provider"

According to the Payment Card Industry Data Security Standard (PCI DSS), a Service Provider is defined as any business or entity that is not a payment card brand (such as Visa or Mastercard) and is involved in the processing, storage, or transmission of payment card data on behalf of another organization. Service Providers play a crucial role in the payment card ecosystem, as they offer various services to help businesses accept and process card payments more effectively and securely.

Service Providers can include a wide range of businesses, such as:

- Payment processors

- Payment gateways

- Hosting providers

- Managed security service providers

- Data storage companies

- Point-of-sale (POS) system providers

- Customer relationship management (CRM) software providers

- Software-as-a-Service (SaaS) providers

Service providers are categorized based on the services they provide and their interactions with payment card data. Here are some common classifications of service providers based on PCI DSS:

|

Level of PCI DSS |

Your business does |

What you should do |

|

2 |

· < 300 000 transactions per year |

· Complete an annual Self-Assessment Questionnaire (SAQ) · Conduct quarterly network scans by an Approved Scanning Vendor (ASV) |

|

1 (Verestro has 1 level of PCI DSS) |

· > 300 000 transactions per year |

· Complete annual internal audit conducted by a Qualified Security Assessor (QSA) · Conduct quarterly PCI ASV scans |

Verestro has the 1st level Service Provider of PCI DSS, which means that we have to go through quarterly PCI ASV scans and an annual external audit performed by certified PCI DSS assessors. In accordance with the principles of PCI DSS, Verestro is obliged to check if the partner is working in compliance with the PCI rules, so we will be checking what the level of transactions and cards in your case is.

So let's remind our two possible scenarios:

Scenario 1 (The partner does not have any access to unencrypted PAN numbers) -> THIS IS THE BEST AND RECOMMENDED SCENARIO. In this scenario you will most likely use our SDKs and admin panel and full encryption of card data. Verestro will guide which Self-Assessment Questionnaire (SAQ A for merchants) is appropriate and ask a few questions (from SAQ). The document will have to be signed by the partner.

Scenario 2 (The partner can access unencrypted PAN numbers) -> in this scenario:

- Verestro will provide a Self-Assessment Questionnaire (SAQ), and ask a few questions. The document will have to be signed by the partner.

- The partner will perform quarterly PCI ASV (Approved Scanning Vendors) scans

(cost around 1k EUR quarterly or less) - The partner can choose any provider from the PCI Security Standards Council (PCI SSC) or Verestro can recommend a supplier. - Until the partner reaches 0,3 mln transactions/interactions annually with PAN numbers, the partner does not need to undergo an annual internal audit (in extreme situations, it is possible to require PCI internal audit from the partner).

If the partner plans to achieve 0,3 million transactions/interactions, there are two options:

- either the partner will move to a scenario that does not touch card numbers using some technology changes

- or the partner should perform an annual internal audit done by a PCI auditor (QSA)

If you would like to discuss your requirements in more detail and receive more information, please contact us.

Thanks for reading.

Multicurrency cards - 3 implementation options

Multi-currency topic is an interesting and important concept of card issuing that usually requires some explanation. Because of the very big market of currency conversion and usually very high fees of universal banks connected with international transactions, it became popular to implement multi-currency cards. Actually the first Revolut use case, heavily promoted several years ago, was connected with this topic. So let's go into details.

There is actually one problem that we want to solve when thinking of implementing multi-currency cards - how to enable the best and most effective card payments in an international environment? There are various approaches to this problem:

Scenario 1 - multi-currency cards and accounts

In this example we offer users multiple payment accounts in various currencies.

- The user gets a single payment card connected with all accounts.

- In case the user pays with currency X, the authorisation system recognises transaction currency and debits account of currency X.

- In case there is no money on this account, system debits another (default) currency.

This example is very often used, but it has a few disadvantages. The first is that the user must perform currency conversion before. It is an action before his/her travel and actually it is an unnecessary action from the logic's perspective. It should be more convenient for the user to have one account and cheap currency conversion during every transaction. But usually consumers like the solution because they can manage this currency problem in advance, see FX rate and can make decisions on how much money to convert.

Implementation of this scenario is not easy because card issuing companies either need to enable multi-currency functionality with Mastercard / VISA or to implement multiple settlement accounts with payment organizations and manage conversions accordingly based on transaction currency. There are additional fees that Mastercard and VISA charge for this service which can make this implementation costly.

Scenario 2 - currency conversion on a single account

Another way of solving the currency conversion topic is to think about how to enable the cheapest conversion during a transaction. In this example the user does not have to convert currency before his travel. He just uses his card while traveling. I personally like this approach the most because it is easier for me but in reality many customers prefer scenario 1.

In this scenario, to have dynamic rates, there is a need for online FX API integration and dynamic management of rates during authorisation. Usually card issuers use static conversion rates offered by Mastercard and VISA but this leads to some additional costs and margins. Ensuring dynamic currency conversion during authorization and proper conversion management may be difficult to achieve.

Scenario 3 - multiple cards for different currencies

The third way of managing the multi-currency topic today in the virtual card environment is issuing multiple cards to multiple accounts in various currencies. In today's world this is easily achievable as the cost of card issuing went heavily down. It works in the way that users have several cards, connected with various accounts and card visuals, visible in Apple Pay or Google Pay with the currency of a particular card. The user can choose a card which is the most convenient for him/her.

In this scenario we need to offer an inexpensive currency conversion mechanism as the user needs to manage balances on each account separately and perform conversion in advance.

This is actually the cheapest scenario of implementation.

While thinking about the multi-currency topic, please consider various scenarios and ways of solving problems. Sometimes the default plan (scenario 1) can be very costly from the transaction processing perspective because of additional fees of payment schemes.

Thanks for reading.

How to prepare for a card issuing project?

Do you want to issue cards to your users? In this article we describe what is required on your side to implement virtual or plastic cards in your applications.

Let's imagine you are a fintech, crypto wallet, lendtech or any other company with a concrete target segment, some or thousands of users and you have a mobile application for your customers. You have decided to go live with card issuance in order to increase revenue and user loyalty. Below we describe the main decisions and steps you need to take to get ready for a card issuing program:

- Decide on a card issuing partner - check out other articles we have on this topic in the Knowledge Center. Make sure that the partner has the necessary functionalities, legal requirements and flexibility that you can accept. Check your partner's financial standing. Contact us for more details.

- Analyse and describe your use cases - describe user flows, develop some initial graphs of how key processes will work. Focus on user onboarding, Know Your Customer steps, card generation and activation, card management and transaction flows. Read the Developer Zone requirements during this step to make sure you are ready to integrate without difficult customisations.

- Check the legal environment - try to analyse and understand the regulatory environment. Check if you can fulfill KYC requirements and how you can collect data from users. It is important that you submit a user selfie and document photos to the card issuer during the verification process. If you are working with us, please make sure that you have a European entity or branch in the EU to sign a contract with us for card issuing.

- Verify API integration - go to the Developer Zone and analyse APIs or SDKs that you will have to connect to. If you want to avoid PCI DSS audits and associated costs, consider using SDKs. It is highly recommended if you have a large group of users.

- Make P&L analysis - consider the revenues from card issuing and the costs of this product. Make sure you understand unit economics. You can use articles in our Knowledge Center to start this work. Choose an affordable partner - do not think that if something is more expensive, it is better in quality. The card issuing business is a cost-based business where low level unit economics matter, especially cost per card and cost per transaction. Revenue share from interchange fees or currency conversions is even more important than costs.

If you have checked these points, you are ready to sign a contract. Contact us sooner, let's work together. We can advise you on many of these points to build the best possible program for you. We have extensive experience in more than 30 countries on 5 continents. Make use of this knowledge to get started.

Thanks for reading.

Card Lifecycle Management

Once launching card issuing projects, our customers usually forget that it is a long-term activity that requires constant verification and improvements. It is very important that you understand and manage your card holders and use best practices in card lifecycle management. Let me summarize key activities from a timeline perspective.

Stage 1 - choosing a card issuing partner

Obvious step. Everybody focuses on financials and technical integration. Very few people check value-added services and other products. Almost no one is aware of PCI DSS & other security requirements that will make your life easier on stage 4 and later ones. Another common mistake is that you do not check the financial stability of your card issuing partner as if it is not important for your business and users.

Stage 2 - implementation

Obviously important. No comments. Check Dev Zone and implement. Make sure your developers read specs carefully. Make sure you understand AML and KYC regulations so that you can comply with rules and the project can be built on strong fundamentals. A common mistake is not to consider Stage 4 - card lifecycle management processes are forgotten.

Stage 3 - launch

Everybody focuses on this moment, plans campaigns, distributes cards. And usually this is the last implementation step of this new product. It is a mistake.

Stage 4 - card lifecycle management

Once you are up and running, it is very important that you are able to monitor your portfolio, create reports, organise personalised campaigns and manage your portfolio in a very active way. There are several rules to follow in order to maximise your portfolio's earnings and performance. The most important ones are summarised below:

- Portfolio Manager - have people that will be responsible for the management of your portfolio. 1 person is enough at the beginning. Make sure these people understand goals and work to make your cardholders active.

- Reporting system- make sure you have a flexible reporting system that gives you information not only about the number of issued cards and transactions, but more importantly on the behaviour of various customer groups:

- have reports how many customers used the card after 1-2 days, be able to find the user IDs,

- have reports with customers that used the card after 5 days, 15 days, 30 days,

- have reports on inactive customer groups.

- Actions - be ready to act basing on the user behaviour

- once you see that your customer is not using the card after 1-2 days - send him/her a notification or an educational reminder,

- once you see that the customer is not using the card for 15 days - maybe you should send a small digital gift to the customer and deliver it if he/she starts using card,

- if you see an inactive customer after 30 days - ask them why they are not using the card; maybe you will get a correct feedback.

- Reporting - again and again check if your actions work correctly. What is their success rate? How are your customers changing their behaviour?

- P&L analysis - make a detailed analysis from a financial perspective, incentivise users to do transactions that are bringing more revenue, think of increasing monthly fees for non-active users.

- Quality reporting - check the quality of your services, ask users for feedback regularly, collect information, analyse it, make actions to improve.

- Value-added services - think of launching new services that can improve performance of your portfolio. Maybe a voucher-based ending, card-to-card money transfers, loyalty programs etc. Ask us for best practices and tools that are easy to use.

- Education (super important) - never underestimate the importance of educational messages. You can teach customers how to use the card on the internet, tell them how to tokenise the card in Apple or Google Pay, show them how to pay at ATMs. Card issuers tend to forget how cheap and profitable it is to work on user education. Do not assume that everyone everywhere uses payment cards the way you use them today. People sometimes do not know how to use 3DS, they are afraid to use it, etc. Work on that.

- Learn, change, improve...

Card issuing is a long-term activity. Please do not think that you will launch it and everything will work properly. You should be constantly working to attract more users and teach existing users how to use the cards so that they add real value to your business. Good luck!

Thanks for reading.

VISA or Mastercard?

Sometimes our customers ask if it is better to issue VISA or Mastercard cards. In this article we would like to answer this question.

Main payment schemes

There are two main payment schemes in the card area that have almost monopolized global card business - VISA and Mastercard. Next to them there are several local schemes, sometimes going global that are also worth thinking of in more sophisticated global projects (like UnionPay China, JCB Japan, EC Karte Germany etc.) but in general in majority of projects you will do the business decision if you prefer to issue VISA or Mastercard cards.

In one sentence the answer is - usually it does not matter. But if you go into details, depending on the country or type of the program there may be some important differences worth considering.

Key decision points

Below we present some important decision points:

- Financial and marketing support - depending on the country and type of program VISA or Mastercard can decide to support your program financially or from some marketing assets. If so, it makes sense to consider this as an important factor in the decision making process. Check with your card issuing partner if there are such possibilities.

- Interchange differences - in some countries (outside of the European Union) there are slight but important differences in Interchange Fees which in the end means that you can earn more from every transaction. Check with your card issuer if such a situation exists on your market. If you are going to offer cards globally, it may also be possible that inter-regional (inter-continental) transactions will be more profitable in one payment scheme. So it is worth checking.

- Cost factors - usually fees connected with a card issuing program will be dictated by your card issuer or BIN Sponsor but in some cases a card issuer may have different fees depending on the cost of VISA or Mastercard transaction fees.

- Special local or global card benefits programs - both Mastercard and VISA are developing various loyalty, discount, value added services that can make your program more interesting for users. In Poland, for example, Mastercard is running a very attractive card benefit and loyalty program called "Priceless Specials". It is worth checking as it may be an important value added for your portfolio and users that may be much more important than any financial details.

- Brand and acceptance - in 95% of countries there is no visible difference in acceptance and brand between VISA and Mastercard. But in some cases it exists. For example if you are going to issue cards in Hungary - Mastercard is much more popular and customers are used to it. It is worth checking before making a decision.

- Educational and consulting support - it can be valuable help. In various projects, countries or regions payment schemes can have services or people that can help you a lot in defining a good value proposition and important details of a card issuing program. This may be very valuable as very often employees of Mastercard and VISA are very professional, have a lot of knowledge and can help you in developing your portfolio. If you have such support, try to use it.

- Shareholding connections - in some cases (like Verestro) one of the payment organizations (in our case - Mastercard) will be a shareholder of your partner. It may be very valuable as you will have in-depth support of the payment scheme and card issuer. It may be useful in various situations, difficult cases connected with rules etc. Make use of such cases, if you can.

Conclusion

Those are the main differences. It is worth considering. In the majority of cases your partner in card issuing will have some preferences and sometimes there will be no choice. But it is certainly worth considering when deciding which card issuer and payment scheme to choose.

Thanks for reading.

Prepaid, debit or credit cards - the main differences

Before launching a card issuing program, our customers consider which card product to use. In this article we will summarize the key differences and considerations.

There are three main groups of payment cards: pre-paid, debit and credit cards. Below we summarize the most important differences.

Prepaid cards

- user has to reload a card account to use a card (like in debit cards by the way)

- you can issue anonymous, non-reloadable gift cards

- in some cases merchants block BINs of prepaid cards more often than for debit or credit cards

- you can have consumer and business prepaid cards

- in many countries, from legal perspective, there is no difference between prepaid and debit cards

Debit cards

This is the biggest group of cards in the world:

- user has to have a payment account or current account connected with a card

- user has to go through a KYC (Know Your Customer) process

- user has to reload a payment account to use card

- usually you cannot issue anonymous cards, because in general they are always reloadable

- sometimes, if you give a loan to your customer, a debit card can work like a credit card

- you can have consumer or business debit cards

- you can have Gold or Platinum debit cards

Credit cards

- user applies for credit and gets it in the form of a card

- usually connected with a revolving credit (something like credit line) and a grace period (no interest for 40-50 days)

- because of the credit, the user needs to go through KYC and credit scoring, so it is more difficult to issue than prepaid or debit cards

- you can have Gold, Platinum or World Elite credit cards

- you can have consumer or business credit cards

- usually an interchange fee is a bit higher than in case of debit cards

- sometimes approval rates for transactions are higher, some merchants (car rental) require credit cards from their customers

- because credit line is connected with this product, usually it is more profitable than a prepaid or debit portfolio

These are the main differences between the above mentioned products. In most cases, you should be thinking about debit cards because they give you the same benefits as prepaid ones, and you can convert them into credit cards by giving loans to your customers.

Tips to avoid problems when implementing card issuing

So you have a good business case for issuing cards for your customers and you found a perfect vendor who can provide formal and technical services in this area. Right after signing the contract you’re ready to implement. What now?

Now it’s time to make sure that the implementation will be as smooth as possible and you and your team won’t get stuck on some of the common problems that may happen in the project. Of course each vendor has his own approach, but let us explain how to avoid some of them based on Verestro’s experience.

Preparing everything for you takes a moment

Depending on your particular setup we will need 4-8 weeks to prepare everything for you. From dedicated environments so that your customers and their cards will always be safe and secure, to ensuring that you will be able to use the cards in Apple and Google wallets and that your proper logo will appear in the 3DS confirmation screen when customers will be paying online. In the meantime you can focus on understanding all the APIs using Sandbox environment and make sure that your team is ready for the work in front of them – for example by analyzing the documentation carefully. Our services will be available for you one by one, so you don’t need to wait full 8 weeks to start implementation – usually first work on your side starts after 2-3 weeks from the kickoff meeting.

Test and adapt

Everyone is always eager to launch the product to final customers – that’s obvious. But it’s good to plan an extensive testing phase that will limit the potential volume of incidents that may happen once you’re live. A simple successful transaction done in ecommerce and brick and mortar POS is a very good prognosis, but should not be the end of testing phase. Take into account different scenarios and edge cases (like reversals and refunds – or even partial reversals). Take into account that there are many players in the world of payments and that a simple transaction is actually a connection of several backend systems (acquirer, issuer, payment network, additional vendors). The more you test, the less surprises will be there in the end.

Knowledge and understanding is key

Issuing cards and processing transactions is unfortunately not like riding a bike – it’s easy to forget. During the project with Verestro you’ll learn a lot about the world of payments and cards. Make sure this knowledge is gathered on your side and distributed between team members.

Plan your MVP

Rome wasn’t built in a day. Best banks did not simply appear in a moment. Issuing cards is a vast topic that requires a lot of iterations to make sure the basics are solid. It’s always good to start with essentials:

- Create user

- Create their balance

- Issue first card

- Digitize the card in Apple/Google Wallet

- Make first eCommerce transaction (with 3DS)

- Make first POS transaction

- Run ‘friends&family’ phase within your company

- Then start adding features and more functionalities

If you’ll start focusing on ‘nice-to-have’ features too early in the process, you may loose sight of more basic processes what may cause delays in the whole project.

Having all of that in mind should make your project more streamlined and effective.

BIN Range or Separate BIN in Card Issuing

Our customers usually ask if it makes sense to issue cards on a separate BIN fully dedicated for a particular project or just use BIN range and share it with other partners. Let me focus on this topic in this short article.

BIN range

There are not so many disadvantages of dedicating a BIN range for your project. In many cases this decision will be much better. Key reasons:

- The project is cheaper as we do not need to implement a new BIN with Mastercard or VISA for you. It is a saving of around 20.000 EUR and monthly maintenance costs are cheaper as well (500-1000 EUR monthly).

- The project is faster for the same reason. It is a saving of around 3-4 months.

- The setup of the BIN range is easier from an operational perspective, so you and we do not consume more mandays for the project.

The only slight disadvantage in such an approach is that there may be a situation when this BIN gets compromised because of some user behavior. It is a very rare situation but it could happen. If you share the BIN with other customers, there is a risk that you will have to change the BIN and cards for customers because of the actions of other customers. We believe that this risk is very small - it has never happened in our history.

Separate BIN

Some people believe that if they have "own" or "dedicated" BIN, the project will be much better. In reality it is not so. It is only more expensive and slower (see above). There is more work and some additional risks connected with the new BIN setup. However, the advantage of a separate BIN is the same as mentioned above - you do not share the BIN with other partners, so in case of BIN compromise, you will know that it happens because of your actions.

I do not see any additional big differences, disadvantages or benefits of using a separate BIN.

Thanks for reading.

IBANs, cards, balances - how to manage all of this?

Once you are starting a payment account and/or card issuing project you need to learn key definitions and relations between those various parameters.

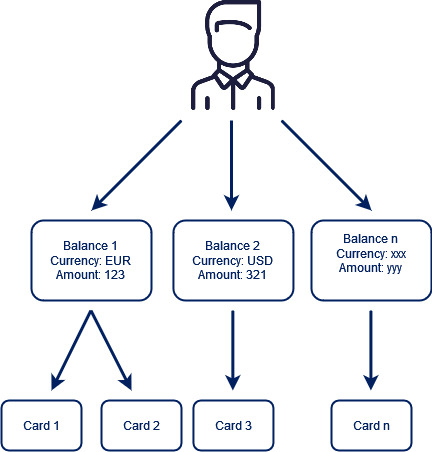

Balance ID - this is a real "account" in the Verestro system. This number is connected with User ID and means that the user has an account and balance in our system. The user can keep money on this Balance ID. Of course, one user can have multiple balances but a single balance can belong to one user only

IBAN - this number is often mixed with Balance ID. IBAN is a number through which the user can receive money to his balance via wire transfer. IBAN is not a balance ID. Generally it does not make sense to have more than one IBAN for one balance. Normally you issue one IBAN for one balance. Usually a user can have more IBANs and balances if he wants to keep money on separate accounts, in various currencies etc.

Card number - easier to understand, just a card number issued to a particular balance ID (not to IBAN!). A user can have multiple cards connected to one balance ID.

Once preparing to project with Verestro, please learn the above definitions. More info here: https://developer.verestro.com/shelves/card-issuing-ibans

Issuing cards in various currencies

Verestro and its partners can issue cards in multiply currencies. Depending on the currency it is easier or more difficult but it is possible to issue cards in multiply currencies. Let me explain how to do it in this article.

Firstly, let's discuss that to issuing cards in particular currency (let's say CZK) means that user has an account in CZK and when he is paying 100 CZK his account gets debited with 100 CZK. To achieve this situation normally the card issuer needs to implement Settlement Service with Mastercard or VISA in CZK. This means that card issuer will have to send 100 CZK to Mastercard after the transaction so that Mastercard could transfer it to acquiring institution and later to merchant. Once this Settlement Service is enabled everything works well but the problem exists if issuer does not have Settlement Service in particular currency or sometimes such Settlement Service does not even exist and issuer must settle money in USD or EUR. Sometimes it is not worth spending money and time on new Settlement Service implementation as it can cost 25-40k euros.

In such situation we can implement Internal Settlement with partner in particular currency. It means that users will keep money in CZK, users will be charged 100 CZK if they pay 100 CZK but all money transfers between Verestro payment institutions and our partners will be happening in EUR. There will be some FX risks connected with this approach but they can be covered through a bit higher fees for users.

There is only one exception to this rule - it is necessary that we can hold money in this new currency in the banks where we hold accounts. It is necessary that accounts are stored in this particular currency to avoid difficult fluctuations.

Ask us for Internal Settlement if you are interested in card issuing in multiply currencies.

What steps should be taken to start a card issuing project with Verestro outside the European Economic Area?

What steps should be taken to start a card issuing project with Verestro outside the European Economic Area?

At Verestro, we are focused on simplifying global fintech space by building a multifunctional, multi-BIN-sponsor, multi-processor, multi-acquiring, multi-bank platform. Our final target is to offer payment and financial services globally in any country in the world. Today we are offering card management, tokenization and payments on 5 continents. We store above 5 mln cards and tokens. In the group we process over 2 bln USD in payment transactions annually.

If you are interested in issuing cards outside of Europe, we can start a project immediately. Normally such a process works in the following way:

1. You contact us and we talk about your plans.

2. You can start integration with our Sandbox immediately using the tech documentation and APIs released in our Developer Zone https://developer.verestro.com/.

3. We sign a contract to cover the services.

4. We search for BIN sponsors relevant for markets where you operate unless we have them already integrated and commercially ready.

5. You can issue cards, enable payouts to cards or enable other payments once you finalize your technical integration and we are ready with the chosen BIN sponsor on the particular market.

6. We take care of all operations, settlements. You take care of your go-to-market strategy, frontend, marketing, pricing, etc.

The big advantage of such an approach is that your platform is not dependent on a single BIN sponsor, you can work with multiple partners. You can also migrate the program easily to your own BINs once it grows and you become a direct Principal Member of Mastercard or VISA.

What are the legal and payment scheme rules for launching a prepaid card program without KYC?

Recently we have been asked the question: “What are the options for a merchant or cafeteria to launch a card program based on prepaid cards (such as lunch cards and gift cards) that doesn't require a KYC process?”

There are a lot of misleading pieces of data regarding prepaid cards and gift cards. Those issues are mainly caused by differences between the legal environment and Mastercard or VISA rules. In this article we would like to go deeper into this topic and explain what is possible and what is not possible.

Key regulatory and scheme requirements for prepaid card programs

Let’s start with key rules:

1. PSD2 (legal environment in Europe) and AML law say that payment institutions have to know their customers so full KYC must apply. Sometimes, depending on the country, some limited KYC rules are possible in case a payment institution issues a payment instrument with payment or transaction limits i.e. non-reloadable gift cards. We work in compliance with the Polish law which states that it is possible to issue anonymous cards only in case:

a. Value of monthly transactions is limited to 150 EUR

b. Value of such card is limited to 150 EUR

c. Only POS and eCommerce transactions are allowed

2. Mastercard and VISA rules claim that in case of specific non-reloadable prepaid cards it is possible to issue anonymous cards. It requires special approval for the program.

3. In some specific use cases (expense management, lunch cards) it is possible to perform KYB of the company selling prepaid cards only. In such a case money on account must belong to the company and the company can issue such cards with limited KYC to its employees or users.

Implementing reloadable and non-reloadable gift cards

Taking the above rules into account, we can imagine the following scenarios:

Scenario 1 – non-reloadable gift cards with limits up to 150 EUR with limited acceptance

It is possible to issue cards for such programs after approval of the payment scheme.

Scenario 2 – reloadable gift cards for the company and its business expenses

It is possible to sell gift cards connected to the business account of the company (after KYB) assuming payments are connected with expenses or specific use cases of this company.

Please contact us if you want to issue similar programs with simplified KYC rules. We will advise on the best scenario and try to find ways to quickly launch a prepaid card program that meets your business needs.

Card Program – in-house or via BaaS?

When launching a new card program, you must decide whether to do it yourself or hire a BIN sponsor or processor and outsource the program to an external entity. This article will address this question, arguing that flexibility and speed-to-market are the most important decision factors.

Let’s start with the definition of a card program and its various parts. Building a new card program requires making decisions in the following areas:

-

Regulatory license – all areas of licensing, relations with the local regulator, anti-money laundering (AML) topics, etc.

-

Card scheme licenses – relations with Mastercard and Visa, settlement processes with Mastercard and Visa, AML and security-related topics

-

Technology – choosing a card management system and/or card issuing processing system. Either in a form of software or a service provided by an external partner. If you are building software in-house, you need to think about software certification with Mastercard and Visa. If you are buying software, you need to think about long-term dependencies on your technical vendors.

-

Security – ensuring compliance with Payment Card Industry Data Security Standards including regular external audits performed by external auditors

-

Card production and delivery – choosing a provider of plastic cards and solving logistic related problems of cards being delivered to users

-

Settlements and collaterals – exchanging money with Mastercard or Visa schemes, hiring banks that need to act as settlement agents, ensuring money is processed on time and all collaterals are paid

-

Operations – ensuring smooth customer service operations including exchange of information with payment schemes, other banks, processing chargebacks & user claims

Building a new card program is almost like building a bank. You need a lot of competences, technology pieces, licenses etc. Obviously, it takes both money and time. It is impossible to run your own card program without 10-20 people being engaged in daily operations, scheme and regulatory compliance, not even talking about technology.

On the other hand, you have the possibility to start a program with a BIN Sponsor or Banking-as-a-Service (BaaS) partner who will be responsible for all those actions. In this case, you will have quick time-to-market but you will have to pay variable fees for those actions.

The answer to which is better is not actually that difficult. In our opinion, the best scenario is to choose a partner with whom you can quickly start (BIN sponsor) and convert your program to a direct license once it grows. This means you can start issuing cards in 3-4 months without high entry costs. You can start building a portfolio and earning first revenue. Once your portfolio reaches around 500,000 cards, it will be worth investing in your own licenses.

Launching card issuing quickly and cost-effectively is critical. While an in-house solution would cost €2.4 million over two years, leveraging Card as a Service (CaaS) / BaaS dramatically reduces both time and initial investment to just €0.2 million, with deployment in 3-4 months. This is the clear choice for agility and financial prudence.

Once you start a project with us, we ensure the flexibility of your development in the long run. We can act as a BIN sponsor and once you are willing to have your own licenses we can either help you in getting a Mastercard or Visa affiliate license or transfer your cards to your own principal membership. Once the cards are issued under your own license, we will act as an issuing processor, and you will only cover technology-related costs. This approach is flexible because it gives you the option to issue cards not only on your own license, but also to use our BIN sponsorship for various projects. This approach offers the best entry costs, the quickest time to market, and highly flexible development scenarios.

If you need more information about our work process, please contact us.

Reverse solicitation – marketing & promotion of card issuing in multiple countries

One of the limitations in global card issuing and account opening activities is connected with licenses and regulations for particular countries. Payment institutions have Mastercard or VISA licenses for particular countries as this is the way Mastercard and VISA systems work. In the European Union it is possible to get a license for the whole region but in other countries and regions you must get a license per country.

This makes the process of card issuing difficult in today’s digital economy because you usually do promotional and marketing activities in multiple countries. You have users from Europe, Asia, Africa, Americas and other continents. It would not be smart to limit your payment services only to users from particular countries.

This is a critical point and you should be discussing this point with your card issuer at the beginning of your cooperation with them. The answer to this problem is not easy or white-black. There are some important considerations that we present below:

- Multi card issuing and multi card processing – we believe that integrations with multiple card issuers that have licenses in multiple countries is critical for the success of global programs. Verestro works with payment organizations in multiple countries and solves this problem globally. In such cases, those problems disappear.

- Regulatory compliance – your payment institution must check if it is legally possible to open a payment account and provide payment cards to users from many countries. In case of our BIN sponsor we are allowed to open payment instruments and accounts to users from multiple countries assuming we fulfill AML requirements

- Mastercard and VISA rules – Mastercard and VISA give licenses for particular countries. It is impossible to get a license for all countries. There are some specific processes to get approval for program in other countries than you have payment scheme license but it is not clear in fact and there are some risks for every program

There are some general rules that you should follow as our partner so let us describe it:

- You should be able to prove that the main focus of your marketing actions is in Europe if your card issuer is based in the EU. We may ask some additional questions. Mastercard can have a look at places where transactions are happening etc. Try to focus on Europe.

- You should be able to provide proof that even if we are distributing cards to consumers living abroad there is an economic interest of those people in Europe. Maybe they travel to Europe, maybe they have employees in Europe etc.

- If you are distributing cards to companies, make sure they have headquarters or offices located and registered in Europe.

- The best would be that your users have resident addresses in the European Union that they are registering during card on-boarding. This solves all the problems.

- We would like to be aware of your marketing activities in countries outside of Europe. It is important that we are aware, maybe we inform local Mastercard so that they are aware.

Our intention in the long run is to solve this problem by working with multiple partners globally and grow with licenses to other countries together with our customers. Don’t hesitate to contact us if you want to do global card issuing business.

Introduction

To meet the needs and expectations of its customers, Verestro has developed a flexible infrastructure, allowing it to issue cards to fintech, merchants, companies, payment institutions or banks. We can provide digital issuing services for licensed payment and banking institutions or using our partner network, BIN sponsors to companies without payment licenses.

Verestro provides its customers with a range of services based on the applicable laws, directives and guidelines of card issuers such as Mastercard and Visa. Meeting these guidelines based on security standards including PCI DSS, 4 steps must be followed to deliver the card to the user:

Create User

The first step to be fulfilled is to register the user in Verestro infrastructure in order to maintain his data in accordance with PCI DSS guidelines and secure the subsequent communication. Depending on the customer's needs to fulfill this step, there is a possibility of delivering a dedicated mobile application or, in case of already existing system, implementing SDK in own application or server-server connection in cases when the application is not necessary. Regardless of the path chosen, Verestro provides its customers with a dedicated Administration Panel to facilitate the management and monitoring of its customers.

White Label Application

To meet the needs of the most demanding customers, Verestro has developed a mobile application for iOS and android. The application has a modular design which, in the shortest possible time, can be personalized to the required functionalities, branded according to the guidelines and published in production. More about this solution can be found in White Label Application.

Mobile SDKs

Customers with their own infrastructure and well-established products who want to provide their users with new mobile functionalities in a fast and easy way, including secure payment instruments, may use dedicated SDKs. Verestro team actively supports their implementation and leads through necessary certification processes. More on SDK based implementation can be found in User Lifecycle & Card Management SDK.

Life Cycle API

Customers who, similarly to the above case, want to expand their offer with competitive functionalities, where mobile application is not applicable, can use dedicated backend solution in server-server connection. LC API created for this purpose in a safe and easy to implement way allows to meet this requirement. More about LC API can be found in User Lifecycle & Card Management API.

KYC

In order to meet the requirements of card issuers, legal regulations and international directives Verestro supports the KYC (Known Your User) process aimed at verification of the customer to whom the services and payment instruments will be offered. As in the case of user registration, here, too, there is the flexibility of adjusting this solution both from the user's side in the mobile application and the processing of the application itself.

Manual KYC Process

The standard Verestro solution makes it possible to collect the necessary data and photos of documents and persons in the mobile application and send the thus prepared request via a secure channel to the Verestro infrastructure. This process is supported both in the implementation of the White Label Application and/or implementation of SDK in the customer application. All KYC data are available through a dedicated Administration Panel, through which the client at a specific access level verifies the data submitted by users.

Automatic eKYC

As KYC process requires customisations and flexibility, Verestro platform enables integration of external entities supporting this process. With the implementation of which it is possible to achieve full automation and thus reduce user verification time to a minimum. With KYC verification automation, the user can have a working payment device within 3-5 minutes of installing the application on their phone.

External KYC

For institutions that are expanding their offerings to include card issuance and already have a KYC process in place, LC API is a dedicated channel from setting KYC status with the user more about it in User Lifecycle & Card Management API.

Create Balance

The third step that brings the user closer to obtaining the card is the creation of a balance / account for the user, which is a dedicated place that maintains the current balance of available funds in a specific currency. Depending on the customer's needs, the user can have a virtually unlimited number of balances.

Automatic

The most commonly used solution is to automatically create the balance as soon as the user gets a positive KYC verification status. With this approach, the user receives the balance in the currency defined within the project.

Manual

A client can create a balance for a user on demand or enable the user to do so themselves. Regardless of the implementation method, the process of creating balances is available in a dedicated mobile application, the provided SDK, from the server-to-server connection and through a dedicated admin panel. More on balance management can be found in Card Management System.

Create Card

The final step is to create a card linked to the previously created balance. Verestro provides its customers with the ability to generate virtual and physical cards for its users. With the implementation of the application in the minimum configuration specified by Mastercard, where the user has a modern e-banking system along with a stylistically attractive physical representation of a virtual card. Processes related to issuing and managing cards are available in Card Management System.

Intro slides

Architecture

API implementation

SDK implementation

Overview

Verestro Card Management System is called ANTACA. The platform provides solutions for creating and managing users' accounts (called "balances"), processing eKYC (user authentication process) and issuing payment cards generated for them.

CMS Antaca provides dedicated services for:

- end-user mobile applications,

- server-to-server connections helpful in integration with existing customer databases,

- administrative panel, necessary from the point of view of financial institutions in the process of issuing cards and managing their clients' funds.

CMS Antaca supports all necessary use cases for various digital and plastic card issuing. It supports integration with multiple issuing processors and can be connected with the one chosen by Verestro partner.

Introduction to Card Issuing process

With the CMS Antaca you can offer your customers two types of cards:

- Virtual card - Digital card without any physical components.

- Physical card – The traditional plastic payment card.

To be able to issue a card for a user, 4 requirements must be met:

- You have to integrated with Verestro platform using JWE token (described below) or other integration methods (API, SDK, White Label).

- User must exist in Verestro database called DataCore. Make sure you register user via User Lifecycle API & SDK.

- User must be strongly verified according to KYC. You can use Verestro KYC (see below) or own KYC process.

- The user must have a User Balance under which the card will be generated.

After those 4 steps you can issue a card for the User.

Below we describe this process step by step:

- Step 1. Configuration & JWE Security,

- Step 2. User Lifecycle API & SDK,

- Step 3. User registration & KYC,

- Step 4. Create User Balance (account),

- Step 5. Card issuing.

Terminology

| Name |

Description |

| Customer | Institution which is using Verestro products. This institution decides which SDK should be used and how transaction should be processed. Basicly Customer can be called Verestro client. |

| User | User which is using Payment Hub Application. It is root of entity tree. User is identified in Wallet Server by some unique identifier which is provided after registration. User can have access to his data and operations based on session. User’s session is created after device pairing is performed. When session expires then user authentication have to be performed. Session is valid 10 minutes, however it is configurable parameter. |

| Card | Card belongs to the user. User can have many cards. Card is identified via internal id given after storing card on Wallet Server. Whole PAN is stored on Wallet Server which has PCI DSS certificate. |

| Device | Device belongs to user. When user starts using application after installation then device pairing is performed. After pairing device with some unique id, unique device installation id is generated and this installation is assigned to user. It is possible to have one active installation on specific device for specific user. |

| Session Token | Token which defines User. It is an authorization way of the User. This entity is created after paring device and this is needed to perform any actions in the application. When session is expired then user authentication needs to be performed. Session is valid 10 minute s, however it is configurable parameter. |

| Sender | Verestro Wallet user which triggers transaction to the Receiver (check User description). |

| Receiver |

Receiver can be identified in Wallet Server (Internal) or may be an entity that does not exist in Wallet Server (External). ◦ Internal – this type of Receiver has his own unique identifier just like sender. It can also act as a Sender in the transaction process, ◦ External – this type of Receiver does not exist in Wallet Server. Transfers that are made to this type of Receiver require the entering of his card data by Sender. |

| Mid | Merchant identifier. This entity is representing Merchant in Acquirer’s system. Customer have to provide the mid information to enable mid configuration in the Verestro system. Required to process 3DS authentication via Verestro System. |

| Acquirer | External institution responsible for processing transaction and 3ds requests ordered by the Verestro Payment Hub App. Acquirer connects with banks / card issuers and returns information whether the ordered action on a given card is possible. |

| PAN | (Primary Account Number) It is 14-19 (usually 16) digits number which is a unique identifier of the payment card issued to the customer's account. |

| Wallet Server | Provides the backend services to support Mobile Payment Application via Verestro Wallet SDK and is responsible for managing users, devices, cards , device tokens, storing transactions history and communication with Acquirers. |