Knowledge Center

You can find more knowledge about fintech and payment products on this site.

- Verestro's Products Overview

- Trends on the Fintech Market

- Why to use Verestro?

- Verestro architecture and choice of products

- Verestro's products for various regions

- What are the Advantages of the Verestro Fintech-as-a-Service Platform?

- Own Payment License or Dependence on a BAAS provider - how does Verestro solve it?

- White-label App vs. In-house App Development

- Mobile App Development Languages Used by Verestro

- Business Control for new or existing portfolios

- What employee benefits can be offered via the Verestro Business Control

- Tokenization and Contactless Payments - Verestro's competitive advantages

- Cashback - Boost Customer Loyalty and Spending

- Understanding White Label Applications: A Beginner's Guide

- How does Verestro differ from standard software companies?

- What is Verestro not doing?

- Tokenize it!

- What is an ACS in the 3DS Ecosystem?

- Card Issuing & Bank Accounts

- Payment schemes

- Ranking of card issuing companies

- Card issuing - financial details

- Example of Profit & Loss calculation in card issuing

- Regulatory and license impact on card issuing

- KYC and KYB requirements in card issuing

- PCI DSS & other security requirements

- Master balance and collateral in card issuing projects

- Pay with Rewards, Pay with Points

- Multicurrency cards - 3 implementation options

- Customer service and user claims in card issuing

- How to prepare for a card issuing project?

- How can I reload a payment account or card?

- Card Lifecycle Management

- VISA or Mastercard?

- Card Benefits in card issuing projects

- Prepaid, debit or credit cards - the main differences

- Tips to avoid problems when implementing card issuing

- Know Your Customer – in-house or outsourcing

- Reverse solicitation – marketing & promotion of card issuing in multiple countries

- Interchange Fees and Service Fees - rates and rules

- BIN Range or Separate BIN in Card Issuing

- Guide to IBAN setup process

- IBANs, cards, balances - how to manage all of this?

- Issuing cards in various currencies

- What steps should be taken to start a card issuing project with Verestro outside the European Economic Area?

- What are the legal and payment scheme rules for launching a prepaid card program without KYC?

- Card Program – in-house or via BaaS?

- Financial Benefits and Costs of Card Issuing Models

- Payouts to Cards & Money Transfers

- Payout to Cards

- Currency Management in Payouts to Cards

- KYC requirements in Payout and Money Transfer projects

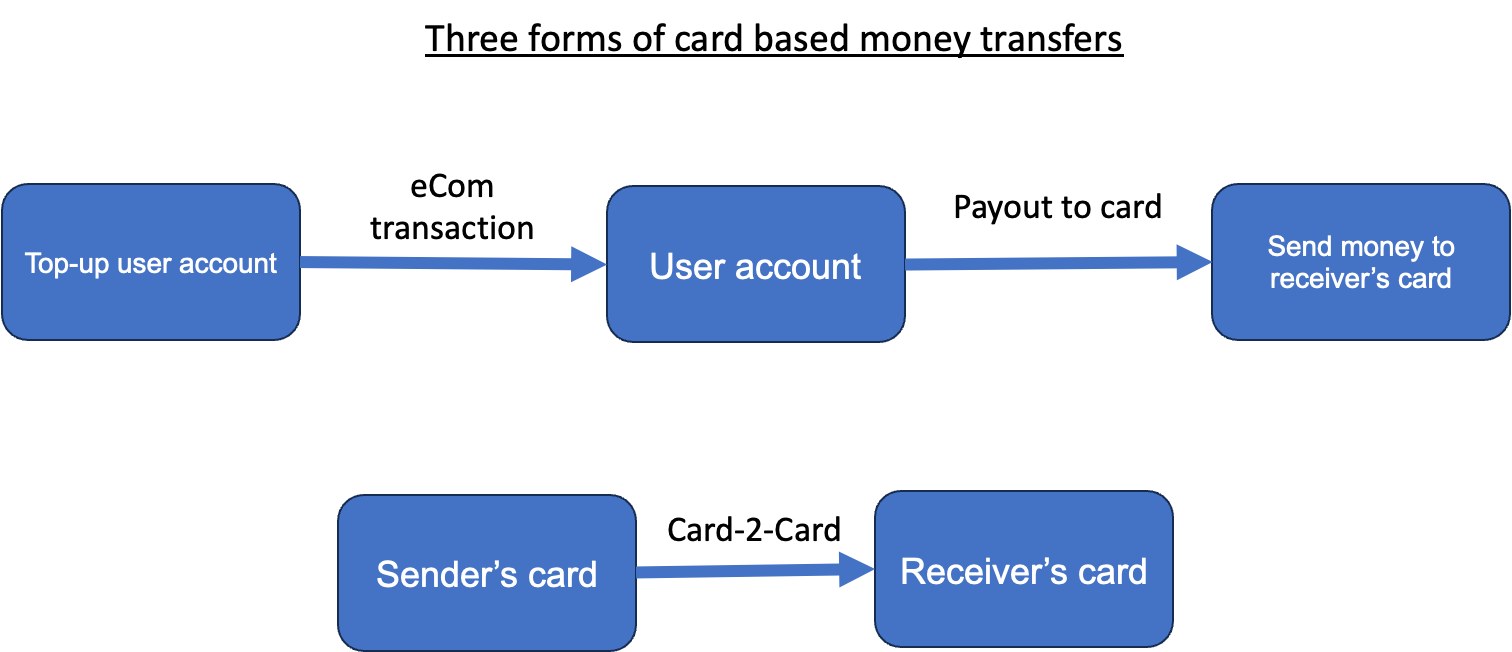

- Various forms of money transfers

- Payouts, eCom Transactions or Card-to-Card Payments?

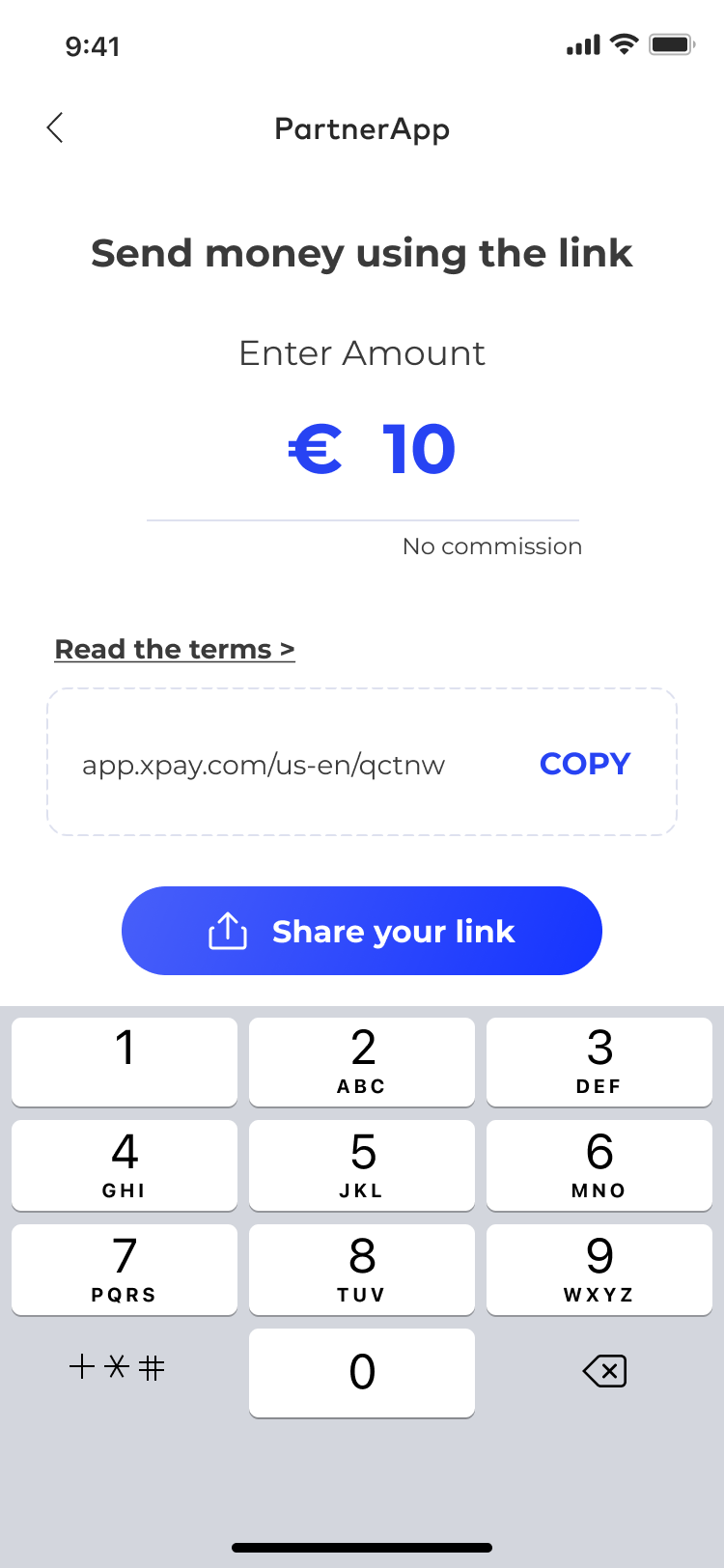

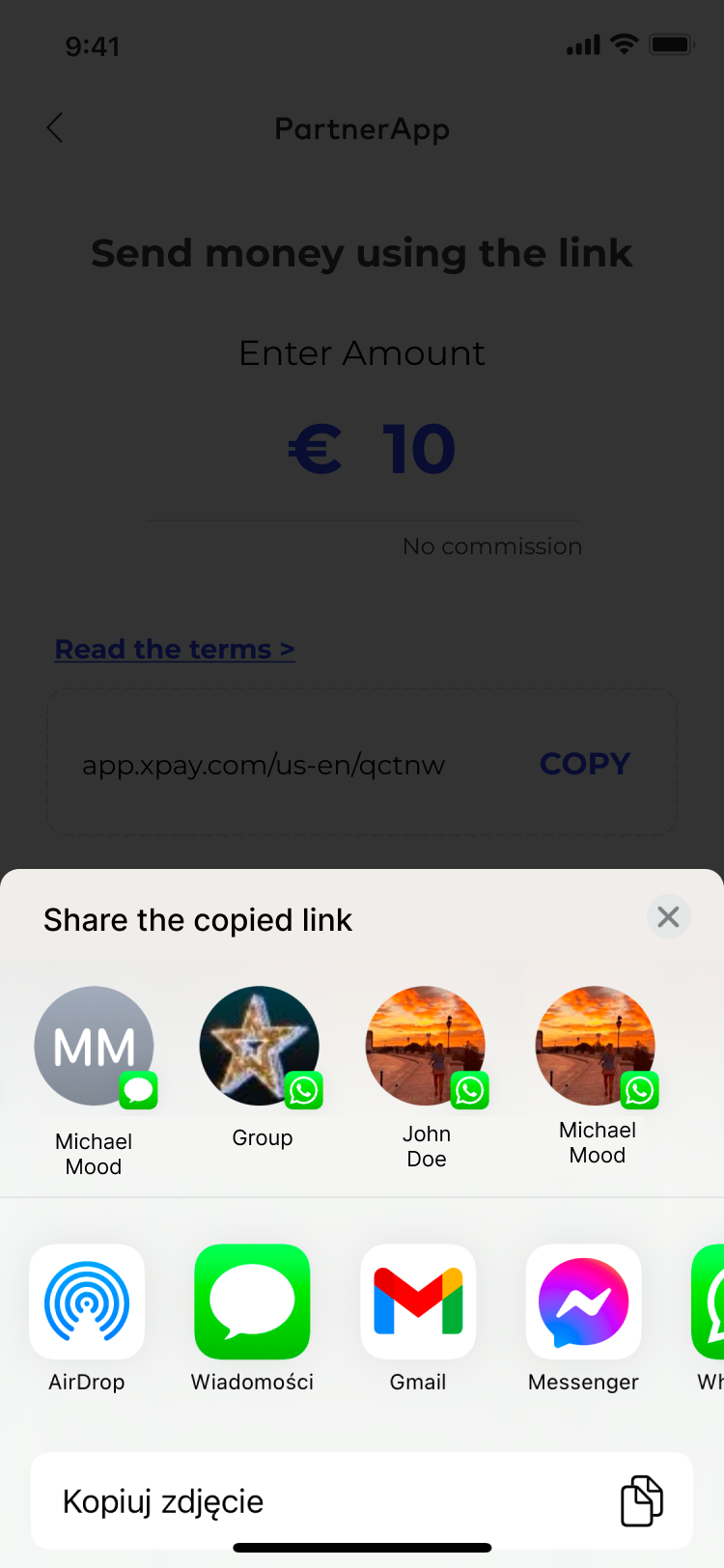

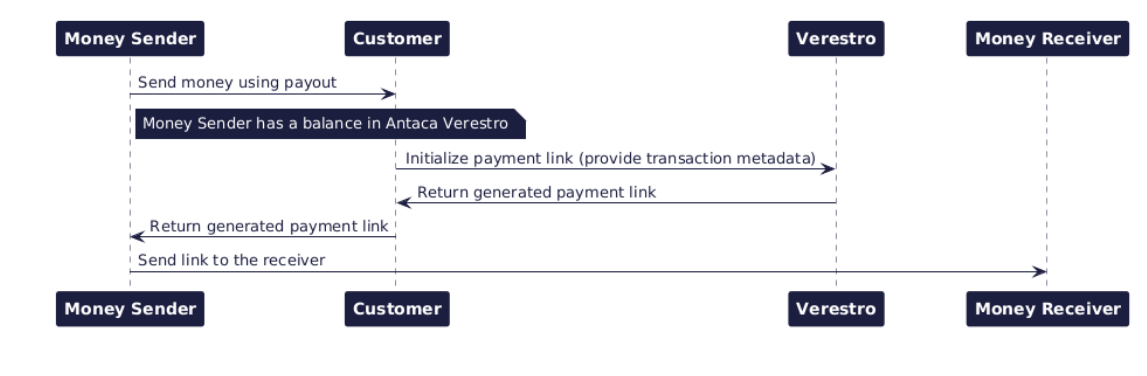

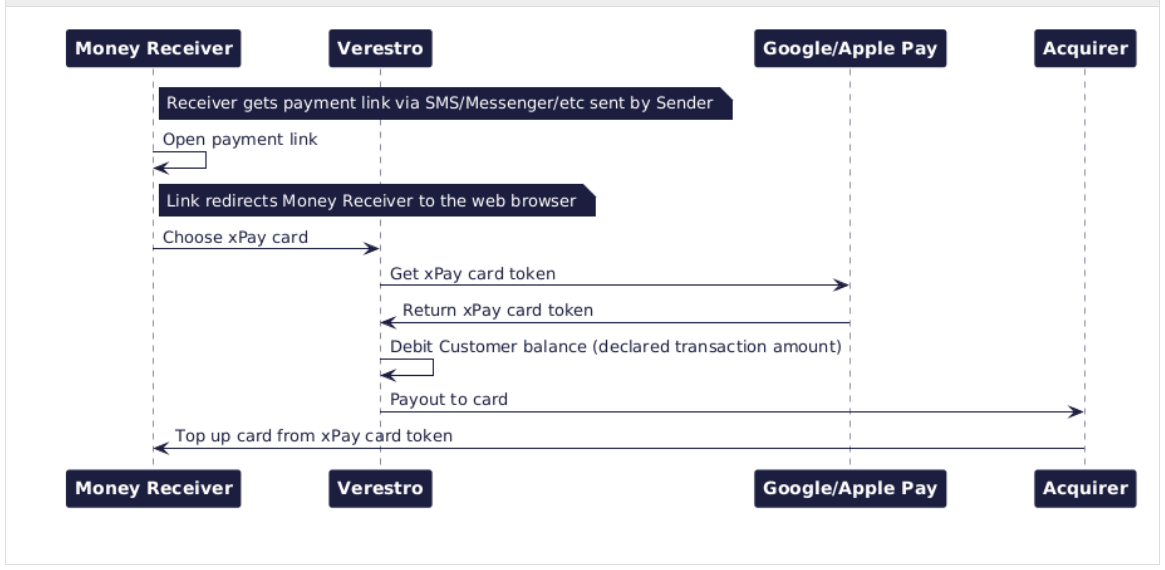

- Payout to xPay

- Card to Card Widget - How Does it Work?

- Cross-Border Card Transactions – Questions about FX Rates and Cash Flow

- Tokenization & Contactless

- Issuer Wallet and Apple Pay / Google Pay - Differences

- NFC on iPhone/iOS

- Pay by Account - NFC from bank account

- On-device tokenization in India

- Push Provisioning Step by Step

- Push Provisioning & Web Push Provisioning

- eCommerce Payment Gateway

Verestro's Products Overview

In this chapter we will present the CEO's view on our products and solutions.

Trends on the Fintech Market

There are various important trends that are impacting the financial technology market at the moment. We try to focus on several of them to stay competitive and propose services which improve user satisfaction, conversion and bring more revenues to our partners. In this article I would like to focus on a few of these ongoing changes:

- Embedded Finance - more and more applications, marketplaces, partners would like to include financial solutions inside their applications. It seems that flexible and not expensive payment solutions are necessary to build a new value proposition in many markets. From lending, through insurance, loyalty platforms, merchants, discount programs, employee benefits - all of them can find useful value in fintech solutions.

- Focus on revenue generation - every financial product must bring value which can be counted in dollars. It used to be expensive to set up a card issuing solution, but it is no longer the case. You can implement and test various financial technologies during 2-3 months. You can have cards with their own visuals, and send money transfers globally easily. Once it becomes easy, all partners focus on solutions that can bring direct revenues per user, per transaction. High cost is no longer a problem today.

- Multi-functionality, multi-acquiring, multi-issuing, multi-processing - there used to be specialised players focused on a particular segment. You had to choose different vendors for card issuing, accounts, money transfer, eCom payments etc. But today it is more and more important to find partners that can offer various solutions, provided by multiple banks, multiple processors under a single roof. Connections between various products bring the most value as thanks to it you can build more sophisticated use cases

- Fraud and AML management - flexible but superior approach to AML, KYC, fraud management is becoming a king. The strategy focused on declining all high risk transactions does not work any longer. Financial players and regulators learned that it is necessary to build rules that enable processing of various types of transactions in a secure way, in line with rules.

- Cryptocurrencies - it seems that after years of ups and downs cryptocurrencies became part of our world. It is difficult to imagine that there will be a hard block for this technology. It is important to start thinking about it as part of financial technologies that bring global value in different use cases.

At Verestro, we focus on those trends to ensure that we can deliver exceptional value for our customers.

Why to use Verestro?

In this article I would like to explain why it is beneficial to leverage the Verestro Fintech-as-a-Service Platform.

Keeping pace in the fintech landscape

Let's start with a description of the problem. Today's financial and payment technology world is a complicated monster. There are new technologies appearing and disappearing every year or even every month. You must invest into new APIs, new interfaces, new frameworks, new security and regulatory requirements. And on the other hand, you have growing costs of IT development. Maybe, during the last years the growth of salaries slowed down a bit but in general one of the biggest costs in your P&L is IT expenditures.

Innovation as a challenge

Let's imagine that you would like to be on top of many innovations in financial technologies. You would like to invest into QR payments, eCom, contactless etc. And you would like to do it of course in high quality. It means that for each of these functionalities you would need a few people to develop and later maintain and host these solutions. A few people means usually 50-100k USD monthly costs for 6-12 months or actually forever. Really forever, because technologies are changing, new frameworks are required, updates are needed.

We think that actually it does not make sense that everybody does it on their own. It would take a lot of time and a lot of money. It is much better and easier if we invest into these technologies and our customers will cover just part of the costs involved in development and maintenance of these platforms. Additionally, we give benefits of compliance with security, legal, regulatory requirements to simplify customers' lives. How does it work?

Verestro’s solution: All-in-One Fintech-as-a-Service Platform

The philosophy is pretty simple. We work on our own, or with Mastercard, with banks, with payment institutions on new products. We are implementing them one-by-one on our platform and thanks to this you are getting a big set of financial technologies in one place. You do not need to manage multiple vendors, you do not need to learn new technologies. You are focused on users, usually you are focused on front-end, core functionalities and your costs are much lower. Our standard fees are lower than AWS or Azure costs of hosting only... but at this price we provide not only hosting but also applications, APIs, connections, regulatory compliance, PCI DSS, business solutions, admin panels, frontend if needed etc.

So, if you want to make use of investments done by multiple parties in the world, get in touch with us!

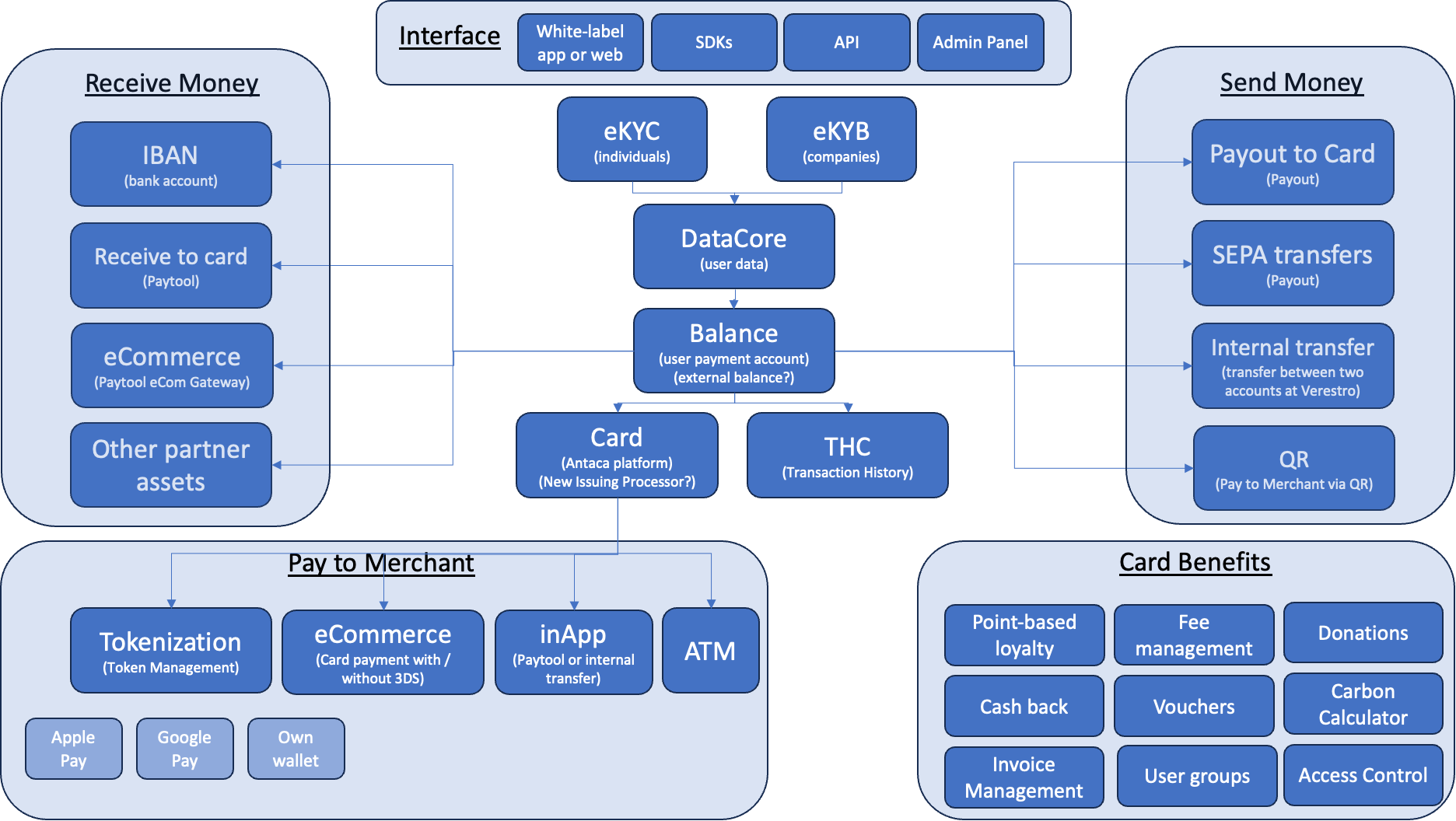

Verestro architecture and choice of products

Below simplified example of Verestro platform architecture. Before every project please decide which functionalities are you going to use.

Please tick bullet points which are needed in your project and deliver it to our sales team:

- INTERFACE

- White-label app

- White-label web

- SDKs - android and iOS, to minimise PCI issues

- APIs

- CORE

- eKYC - are you going to register consumers? do you have own KYC solution or want to use ours?

- eKYB - are you going to register business customers? do you have own KYB solution or want to use ours?

- Data Core (any user data will be delivered to Verestro) - almost always needed

- Balance

- Card - do you want to use our issuing processing capabilities or you have another issuing processor

- Transaction History

- RECEIVE MONEY

- IBAN for receiving

- Receive to card

- eCommerce gateway - do you want to use our acquirer or you have another acquirer? which ways of payments?

- Other partner assets - do you want to reload cards with points, digital assets etc.

- SEND MONEY

- Payout to Card - sending money to any VISA or Mastercard card?

- SEPA transfers

- Internal transfers between our accounts

- QR payments

- Other ways of sending money?

- PAY TO MERCHANT

- Apple Pay

- Google Pay

- Own wallet

- eCommerce payments

- inApp payments

- Payments from own wallet

- ATM

- CARD BENEFITS

- Point-based loyalty

- Fee management

- Donations

- Cash back

- Vouchers

- Carbon Calculator

- Invoice management

- User groups

We are constantly adding new value added functionalities. Check if we have not added something new in the meantime :) Contact us.

Verestro's products for various regions

Our mission at Verestro is to provide cutting-edge fintech technologies and make them affordable to everyone. We work with banks, fintech providers, payment schemes, payment gateways, merchants, corporations and small businesses and develop a BAAS / FAAS platform. However, as "payments" is a regulated business, we are not able to provide all our services globally at the moment. Below we describe key products we distribute in particular regions.

- The European Union

- Key customers: banks, fintech, payment providers, merchants, businesses, insurances, lendtech etc.

- Key products: all products described in our Developer Zone, including technology and regulated payments solutions.

- Taking into account market dynamics, our key focus is on:

- North & South America

- Key customers: banks, processors, payment schemes, fintech.

- Key products: we are focused on selling technology platforms because we do not have a payment license at the moment; we do work with various partners like Paymentology or Girasol to provide end-to-end payment solutions; we can offer payment accounts and cards in Europe if customer has office in Europe.

- Taking into account market dynamics, our key focus is on:

- East Asia incl. India

- Key customers: banks, processors, payment schemes, fintech.

- Key products: focus on technology products around tokenization and money transfers; we can offer payment accounts and cards in Europe if customer has an office in Europe.

- Taking into account market dynamics, our key focus is on:

- Middle East & Africa

- Key customers: banks, processors, payment schemes, fintech.

- Key products: focus on technology around tokenization and white label; we can offer payment accounts and cards in Europe if customer has office in Europe:

What are the Advantages of the Verestro Fintech-as-a-Service Platform?

Each time we approach our customers, we are asked what advantages over the competitors our solution brings. In this article I would like to describe a couple of points which differentiate us among this pot of financial technologies vendors.

Advantages of the Verestro Fintech-as-a-Service Platform

1. Speed

200% faster than building everything in-house. Instead of building every fintech product yourself, You can use our platform and You will have all of those services much faster and at lower investment costs. Let’s take card issuing for example. To start issuing cards You need to cover very costly and time consuming areas. You have to:

- build Your architecture and its individual components like data core center to manage cards, '

- have all kind of backends to tokenize the cards,

- create admin panels,

- integrate with Mastercard or Visa platforms,

- create the SDKs to integrate them with Your mobile interface,

- finally find or build Your own processing facility,

- and obtain a license of an official payment institution.

It may take from 1,5 to even 3 years and cost You a fortune counted in millions of euros! Choosing a Fintech-as-a-Service model is way more efficient as You simply do it all in 3 months.

2. Cost-Effectiveness

Our services cost up to 50% less than those of the competition! Often customers complain of high costs of fintech services. The cost of implementing our fintech services is one of the lowest in the industry, due to the maintained cost discipline, the location of the software house in the relatively cheapest country in the EU in terms of personnel costs, and the accumulated experience of more than 65 completed implementation projects.

Thanks to the subscription-based Fintech-as-a-Service sales model, the cost of our services is also significantly cheaper than the cost of developing such services in-house. As in the above-mentioned example of card issuing, the cost of card issuing program may exceed 1-2 m euros where in fintech-as-a-service case You will be only charged for a setup fee not higher than 20 k euro and then You will need to pay a monthly fee for the maintenance dependent on the type of cards You issue 4-8 k euro per month. Isn’t it a good deal?

3. Long-Term Financial Stability

We are profitable, no loans, not dependent on investor money. We have Mastercard as a shareholder. You get a partner with long term financial stability which is extremely rare in our industry. Before signing any agreement with any vendor of financial technologies please make sure You double checked their financial condition usually available in the investors tabs on their official websites. You don’t want to wake up one day with Your customers cut off from their payment cards.

4. Flexibility

Direct contact and flexibility! At Verestro,You get in touch with decision makers and we are ready to listen to Your needs. As long as You are not violating financial, AML rules - we are happy to be flexible and update our rules to Your needs.

Even though we would prefer to sell our off-the-shelf products like card issuing, tokenization, money transfers or a business expense management system, we all know, sometimes, some customisations are simply unavoidable. We have wide experience in tailoring the products to our Partners' needs.

5. New Revenue Streams

Generate new revenue with our fintech products! Our clients value rapid implementation of fintech services because it allows them to start generating revenue or reduce costs faster from such services as payment card issuance and cross-border transfers, online payments.

Based on our experience and optimized processes and API/SDK ,it takes 4 times less effort to launch new products and start generating revenues on them. One of the good examples of the way You can quickly start earning on Your payment cards is a Fees module. Simply set up the fees on each issued card and start to earn from the first day of the project.

Contact

If You want to challenge some of the above-mentioned statements, feel free to book a call with one of our sales representatives at sales@verestro.com. We look forward to hearing from you!

Own Payment License or Dependence on a BAAS provider - how does Verestro solve it?

If you are a fintech provider, there is one single risk of choosing a BAAS partner - long-term dependence on a regulatory license of the partner. We will focus on this topic in this article and explain how Verestro's proposal differs from all other BAAS providers.

At the beginning of your fintech journey, there is usually not enough time to cover all the topics and build every single payment license yourself. In fact, it does not even make sense. Therefore, fintech start-ups and scale-ups usually choose BAAS partners and develop their business with them.

Such a decision is actually an important risk for every fintech because you start being dependent on BAAS partners. Your customer gets registered to accounts and payment services of your partner and in the long run you are building a serious risk for yourself. Maybe you do not care about this problem at this stage but think of it. It is a super important risk. What can happen:

- Your BAAS partner may increase prices and you will have to pay

- Your BAAS partner has problems with a regulatory institution and you must follow new rules that regulator is pushing to the payment provider

- Your BAAS partner has AML issues and your BIN, your cards are blocked because of other customers

There are many risks. At Verestro, we solve this problem in various ways:

- We are not only BAAS but also technology provider - a lot of our projects are performed in cooperation with banks, payment institutions where we act as a technology provider only. We can also do it for you which means that once you get your own payment license, we can use the same technical infrastructure to issue your cards and open your accounts.

- We are not dependent on a single payment institution - we work on multi-issuing, multi-bank, and multi-acquiring solutions, so that you can have a choice of payment institutions that you work with. It is a unique functionality of our platform. It enables you to work globally with multiple payment institutions or to switch payment partners once it is necessary for your business.

- We work with multiple banks - we have cooperation with many financial institutions and banks all over the world and our core strategy is to bring you accounts and payments in all countries. You can choose IBANs and BINs from various countries. You can choose currencies, local payment solutions etc.

In conclusion, when you choose Verestro, you get long-term stability and a solution to this important risk. Contact us for more details.

White-label App vs. In-house App Development

In the world of growing IT development costs, our customers are asking more and more questions regarding white label frontend and mobile app development. In this article we will focus on the most important advantages and disadvantages of using white label frontend products.

Introduction to app development

Let's start with an introduction. As a company willing to launch new fintech products or willing to implement a mobile application for your users or employees, you need to make a business decision on how to implement it:

- Your own development (in-house) - in this case you will hire developers, choose a front-end technical framework and will work with your team to implement a mobile app fully dedicated to your business.

- Choosing a white label product - in this case you have to choose a vendor of a white label application, learn how to customise this application and eventually hire a team that will work on customisations necessary for your business use cases.

This choice is actually a super important decision that many business people underestimate. Let's focus on the key advantages and disadvantages of working in both models.

Scenario 1 - In-house app development

This is a common scenario for many banks, new fintechs, corporations, etc. It seems to be very easy. You will hire one or two developers for a few months and after this period of time you will have a perfect product that will include multiple functionalities. You can then resign from developers and have great business use cases for your customers. To hire developers you will usually try to hire an external IT outsourcing company that will promise to you that it is easy, fast and inexpensive.

Nothing in the above sentences is true! :) Really nothing. Many business people, especially company managers, think that front-end development is easy. That everything works great on any type of phone and that integrating backend APIs is super easy and fast.

Disadvantages

In reality, it takes time. A lot of time. To have a very good front-end product built from scratch, without bugs, you usually have to plan 12-24 months of constant development, tests, changes etc. And after this period you cannot resign from the development team. You need to have people that will work on changes, updates, will implement technical updates required by Apple, Google, security rules etc. Let's do a quick calculation. The smallest IT team today consists of 4-5 people: backend developer, frontend developer (one or two depending on chosen technology), tester, product owner / scrum master / project manager / UX person. If you want to have fast development, this team should be bigger (8-10 people). Additionally you need hosting services - AWS or Azzure can quickly become a large part of your cost structure. You need additional software and systems connected with development work, such as Slack, Jenkins, Kubernetes, etc. All of this costs money. In short, you should expect the following costs:

- 5 people * min. 6.000 EUR average cost = 30.000 EUR monthly

- 5.000 EUR hosting monthly

- 1.000 EUR additional costs

- not including office costs, bonuses etc.

TOTAL: 36.000 EUR monthly cost -> FOR THE SMALLEST POSSIBLE TEAM!

And let's imagine that you have to spend 10 months for MVP development -> 360.0000 EUR one-time fee.

It is the cost you have to cover just to implement your MVP. Without any marketing, without any customer reactions, no sales during the period. In reality I think that you should assume that this cost of doing the implementation in such a way is 2-3 times higher than this minimum cost - almost 1 mln EUR.

Additionally, you should take into account that development done by a very small team requires technical compromises. Most likely you will not use Native iOS and Android technologies that are the best from UX perspective. IT companies will recommend to you various hybrid technologies which is always a compromise in the UX area. You will also not gather experience from other projects done in similar areas. Your mistakes will usually be first mistakes, your developer mistakes will require updates, etc.

What's even more important, you need to think about long-term development, hosting and maintenance costs. Maybe you can limit the team by 50% but costs of hosting will grow for sure with new users coming to your system. I would assume that you will have a monthly cost of 10-20.000 EUR to cover to keep the application running.

Advantages

Apologies for describing so many disadvantages but I think it is true. However, there are big advantages. If you can afford those costs and time spending, you will have full freedom. You can do with your app whatever you want to do. You can implement new features, change everything, implement new technology quickly. The dependency is only on your budget. I fully admit that this is a super important advantage that can be strategic for many start-ups and companies. I am just not sure that you must get this advantage at the very beginning of your project. Sometimes cost and time is much more important than full freedom of development. Go-to-market time may be decisive for getting new investors, growing revenues will be critical to proving that there is a problem you are solving.

Scenario 2 - White label application

Using a white label application is another strategy you can choose. In such a situation the majority of components of your application are already developed. You use an already existing product that can be customised to your requirements and you hire your developers just in case you want to make various non-standard changes in the app.

The following rules for choosing a white label application vendor are very important:

- Carefully choose technology - please remember that native iOS and Android solutions are just better from the UX and performance behaviour. This is what Apple and Google use for their apps.

- Check the possibility of customisations - make sure you understand flexibility of the product, if you can add new features, if your developers can work on the code, if you can change just colours and logo or the entire look and feel in the long run.

- Verify experience - check examples of other customers using this product. See how they look like, test them.

- Prices - obviously important. Remember to check both one-time and on-going maintenance prices. The 2nd ones are even more important.

- Intellectual property - very important. Is it possible that you get full IP rights to the copy of your application. Would you be able to change the development later to your own development.

- Security and financial stability - make sure you work with a partner that is financially stable and will not close your project in the middle of the development.

These are the most important issues that you need to check. Once you check them and they are acceptable for your business, you may get a result that your product can be 5 times faster on the market, costs can be 4 times lower, revenues will appear much faster etc. Today, the cost of white label applications can be as low as 40-60.000 EUR for development. The maintenance - 4-5.000 EUR. It can be critical for the business, especially during the first phases of growth.

Summary

I recommend that you do not believe that the world of front-end development is simple and inexpensive :) Do not make this mistake. Consider carefully if you have enough time and money. In fact, one of the most important aspects of project development is the comparison of revenues and costs. Costs are known for sure. Revenue is usually unknown. Make sure you do not overinvest. It is very easy to make a decision that you want to spend half of your 2 mln EUR on technical solution but actually it will be much, much better if you spend 200.000 EUR on a technical solution and the remaining 800.000 EUR will be used for promotions, marketing, user acquisition. This usually matters the most.

Anyhow, good luck. Thanks for reading.

Mobile App Development Languages Used by Verestro

This article summarizes programming languages & technologies we're utilizing to build our mobile solutions.

Why should I care?

If you want to use Verestro's SDKs in your mobile apps or you are interested in our Whitelabel Mobile Application, with intention of future maintenance by your own team, you may want to check if our products fit your technology stack well.

Native solution

Most of our solutions for mobile apps leverages technologies native for each mobile platform:

- For Android - Kotlin (seamlessly works also with java-based projects)

- For iOS - Swift

This enables best performance, security and integration of platform-specific features. You may also create your own native SDKs for your products that will work with our ecosystem. More details available here.

Compatibility with web-based solutions

It is possible to embed widgets or entire web-based screens inside our Whitelabel Mobile Application. We'll pass you data about the currently signed in user, so you can display relevant information. More information about it is available here.

Flutter, React Native and other cross-platform tools

While we don't provide SDKs for mobile apps written in Java Script & Dart, our native SDKs work great in such an environment. Both most popular cross-platform frameworks include relevant solutions for this:

- For Flutter you use Platform Channels

- For React Native you have Native Modules

Business Control for new or existing portfolios

One of our important products is Business Control. You can find more information about this solution under the following link - Business Control

Our customers are asking us from time to time if it is possible to use Business Control for the existing portfolio of customers and cards or if it is aimed for new customers. Let me clarify this topic in this article.

Business Control is a platform or set of functionalities targeted at business customers that should give them more control over spendings, company expenses, cost and invoice management and more. Verestro offers it to banks and fintechs as a technology platform or we also can deliver it directly to corporations in connection with our partnering payment institutions in various parts of the world.

It offers several important benefits for business customers:

- super easy issuing of virtual cards for various company expenses - imagine that your manager can issue a virtual card to you when you go to a conference in another country. Card will be valid for 2 weeks, will have various limits etc.

- invoice management - instead of collecting pictures or doing photos you just scan an invoice and it lands directly in finance or accounting department for approval and further processing

- employee benefits - you can use cards with multiply visuals to give Christmas gifts or Valentine Cards or Thank You Gifts to your employees

- all the money is held in one or a few payment accounts which means that you do not need to pre-paid every card. You keep money and deliver "limits" to your users. It is a very important benefit vs pre-paid cards.

Let's imagine that you already have a portfolio of business customers because you are a bank or fintech partner and you would like to offer such a platform to your customers. Quick answer is - of course it is possible to offer Business Control to your existing customers.

After some integration and implementation projects you will give your existing customers an opportunity to issue new virtual cards for their employees, manage invoices and expenses etc. However, take into account that if you would like to enable it for already issued cards, actually you are using just part of the functionalities. The card already exists, it is in hands of the user, so in fact it means that you will not issue a new card for this person but you can:

- manage limits of cards

- manage invoices

- have new interface for company / employee

- and additional possibility to issue new virtual cards for this company or business customer

Feel free to contact us and discuss details of such implementation.

Regards,

Krzysztof

What employee benefits can be offered via the Verestro Business Control

Our Business Control platform provides the opportunity to issue virtual cards and manage business expenses. But in fact it can be used in multiple ways for companies. Here are a few examples of such use cases:

- Business payment card - your employee going for a trip, conference, meeting with a customer can get a virtual payment card and use it for payments globally. Once the employee makes a transaction, he/she can scan an invoice and connect it with the transaction so that the finance team and accounting have an easier process of expense management. This is a usual use case.

- Salary card - you can send salaries to your employees worldwide by using Business Control. If you issue a card with a specific limit to your employee, the employee can start making purchases and use it as a normal card. Thanks to it you have an easy salary transfer mechanism to all employees globally.

- Lunch card - you can issue cards for your employees and offer them a virtual card as a lunch card to get some tax benefits (depending on the country). Thanks to Business Control you can limit the acceptance of these cards to dining so that employees could use the cards for meals.

- Gift cards, holiday gifts, Thank You Card - you can issue a virtual card via Business Control any time you want to reward a particular behaviour of your employees. It is a bonus for the employee. You can have a specific "bonus" or "holiday" related card visual, you can add a message to the employee so that he/she knows that this card is for the particular achievement.

- Limiting time for expense processing in the company - if you want to limit hours spent by your employees, administration, finance and accounting teams for expense processing, finding documents, connecting them with transactions, etc., you can use Business Control. We can integrate Business Control with your ERP system, we can transfer invoices and transaction data to your internal databases so that transactions can be processed automatically. Think how many hours you lose every month of such manual activities connected with expense management.

Please remember that we offer this product through partnering with payment or banking institutions. We can also offer it directly to companies in Europe. Contact us if you want to know more about this product.

Tokenization and Contactless Payments - Verestro's competitive advantages

The most important reason why you should use the Verestro Tokenization and Contactless Payment Solutions

There are many reasons why to use Tokenization and Contactless Payment solutions provided by Verestro but one of them is definitely the most important. We can give you access to ALL ways of NFC and contactless payments through a single platform and one vendor. There are multiple partners you will have to integrate with and certify. Some processors will enable the majority of them but very few will give you access to all. Some IT companies will tell you that they can do everything and connect to everyone but it is also not true. It takes time and money to get new integrations and certifications.

Examples of questions that you can ask your vendors

- Imagine that 10% of your users are using Huawei phones. Are you ready to provide contactless payments to their phones now?

- What if many of your users have cheap Android phones? Will your solution work on this? How many MB are used by your system (in our case below 4MB)?

- What if you are issuing cards in multiple markets? Is your current solution ready globally?

- What if you are planning to tokenize bank accounts (not cards but bank accounts) - is your platform ready for this?

Verestro's solutions

At Verestro we solve this problem by certifying and standardising integration with all possible ways of payments. We are delivering our tokenization and NFC cloud payment platform globally to multiple bank and payment institutions. Current list of certified solutions is:

- phones: Apple, Huawei, Pixel, Samsung, LG, Motorola, Xiaomi etc.

- operating systems: iOS, Android

- X-pays: Apple Pay, Google Pay, Samsung Pay, Fitbit Pay, Garmin Pay, your own wallet, your own X-Pay

- payment schemes: VISA, Mastercard, Pay-by-Account, Local scheme

- countries: global, possibility of local data hosting or transaction processing

Business benefits

Additional business benefits that make us unique are:

- possibility of registering individual card visuals

- delivering the full scope of reporting for Apple and Google inside the Verestro Token Management Platform

- possibility to organize card registration to Apple or Google with own, proprietary CVC / CVV verification method (no need for integration)

- cheap and quick - below 20k eur one-time, below 4k eur per month, 2-4 months only

Please contact us for more information.

Cashback - Boost Customer Loyalty and Spending

In today's competitive financial landscape, cashback has emerged as a game-changing strategy for businesses looking to attract and retain customers. But what exactly is cashback, and why should your company consider implementing it? Let's dive into the world of cashback and explore its benefits and versatile applications.

Why Should We Use Cashback?

Cashback is more than just a perk – it's a powerful tool that can transform your business. Here's why:

- Enhance Customer Loyalty: By offering a percentage of money back on purchases, you create a compelling reason for customers to choose your service over competitors. This incentive encourages repeat business and fosters long-term relationships.

- Boost Customer Spending: The prospect of earning cashback motivates customers to spend more. It's a win-win situation: customers feel they're getting more value, while your business sees increased revenue.

- Gain a Competitive Edge: In a crowded marketplace, cashback can be the differentiator that sets your product apart. It's an attractive benefit that can sway potential customers in your favor.

- Real-Time Gratification: With immediate calculation and allocation of cashback after transactions, customers experience instant rewards, reinforcing positive associations with your brand.

- Flexible and Customizable: Cashback programs can be tailored to suit your business model and customer preferences, allowing for targeted promotions and strategic incentives.

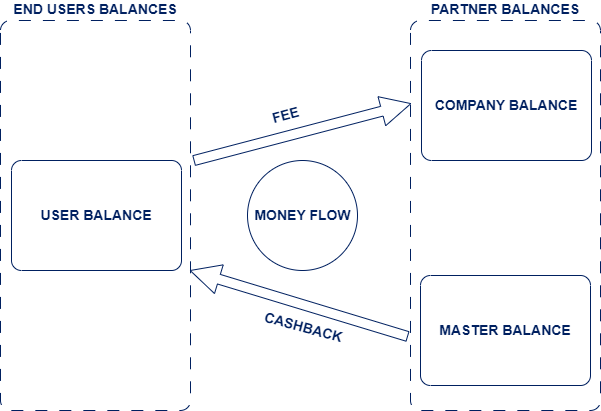

Cashback & fees money flow

Cashback is an internal transaction for a partner who wants to top up the user's balance as part of the loyalty program.

Our card & balances management system (Antaca) automatically debits the masterbalance with this transaction.

Cashback Rules: How to Maximize Your Rewards

The true power of cashback lies in its flexibility. Here are some innovative rules and use cases you can implement:

- Percentage-Based Rewards: Offer a consistent cashback percentage on all purchases (flat rate), such as 0.5% cashback on every transaction. Alternatively, implement tiered rates to reward bigger spenders, like 0.2% for transactions up to $100, and 0.5% for transactions over $100.

- Fixed Amount Rewards: Provide a fixed cashback amount for each qualifying transaction, regardless of the purchase amount. You can also offer different fixed cashback amounts based on transaction value ranges.

- Merchant-Specific Cashback: Boost partnerships by offering higher cashback rates for specific merchants. For example, 2% cashback on purchases from your partner stores.

- Category-Based Rewards: Encourage spending in particular sectors by offering higher cashback rates for specific transaction categories. For instance, 3% cashback on all bookstore purchases (MCC code 5942).

- Payment Method Incentives: Promote certain payment methods by offering higher cashback rates. For example, 0.5% extra cashback for transactions made with Samsung Pay.

- Geographical Targeting: Encourage local or international spending with location-based cashback rules. Offer 1% cashback on all transactions made within the EU.

- Currency-Specific Rewards: Incentivize transactions in specific currencies, such as offering 0.75% cashback on all USD transactions.

- Time-Limited Promotions: Create urgency with limited-time cashback offers. For example, double cashback rates during holiday shopping seasons.

- Cumulative Rewards: Reward loyal customers with increasing cashback rates based on their total spend over time. For instance, unlock 1% cashback after $1000 in total purchases.

Cumulative Rewards feature needs implementation.

How to implement cashback?

Please feel free to contact us and we will setup various cashback rules on Verestro platform for you.

Please make sure you build your cashback network with partners, merchants etc.

It is not part of our responsibilities at the moment.

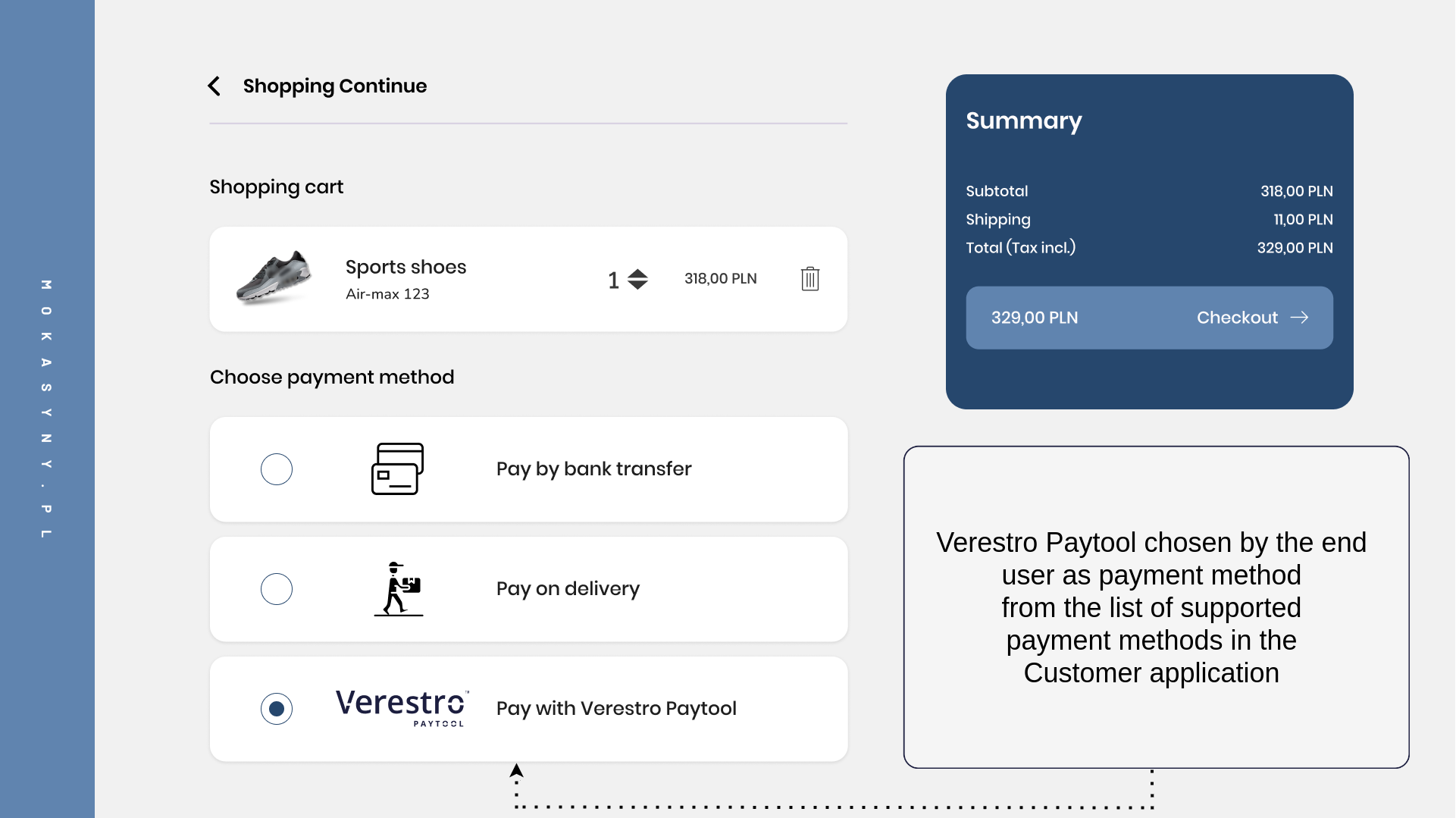

Understanding White Label Applications: A Beginner's Guide

Our clients often search for effective ways to scale their offerings. The obvious way to do this is to create their own product through the entire production process, from identifying the market and its trends, to building a prototype and implementing the system, to continuous improvement. This approach requires a lot of resources and time. However, it is worth asking ourselves whether we are able to take such risks? What if the product is finished, once the demand for such solutions in the market starts to fade, or by the number of competing solutions it becomes difficult to achieve the desired results? Perhaps better results will come from using proven solutions created by experts who know the trends and have solutions in their portfolio that have paid off in the market. Due to the factors mentioned above, investors are increasingly using white label applications.

What is a White Label Application?

At its core, a white label application is a pre-built software product that can be rebranded and customized by businesses as their own. Think of it as a “ready-made” app that developers create, but the final product is branded with your company's logo, design, and name. The white label provider handles the coding, updates, and maintenance, while your business gets a fully functional application under your own brand. You don't have to worry about required security certifications or updates for new iOS/ANdroid versions.

How Do White Label Applications Work?

Here’s a simplified step-by-step process of how white label applications typically work:

- Purchase or License the Software: Buy the application or license for a pre-developed app.

- Customization: Customize the app by adding branding elements, such as logos, color schemes etc. and add your core product features through widgets or new screens.

- Launch and Market: Once the app is branded, it is ready for deployment. The business can now offer it to customers as a proprietary solution.

During the customization step mentioned above there could be small and complex customizations. This is usually the critical topic how deeply you can influence white label so that it fulfills customer needs. Let's go deeper on this topic.

What is considered as custom development in the context of White Label?

Custom development involves deeper, more technical modifications to the core functionality of the white label application. This goes beyond just changing the look and feel of the app; it involves altering or adding features, adjusting workflows, or integrating the app with other systems. In essence, custom development changes the app's functionality to meet specific business requirements.

Key Characteristics:

- Feature Enhancements: Adding new features or modifying existing ones to meet unique business needs (e.g., integrating custom payment gateways, modifying end-user flows, etc.).

- Technical Adjustments: Tweaking or rebuilding parts of the app's code to support new functionalities, or to change behaviour.

- Custom Integrations: Integrating the app with third-party tools like CRMs, webviews or other business platforms.

- API Integration: Developing custom APIs or integrating the app with existing APIs to communicate with other services.

- Data Handling: Modifying how the app collects, stores, or processes data.

Example: The company buys a white label app but wants to add a custom fitness tracker, integrate it with their gym's membership system, and implement push notifications. This is the custom development.

What is considered as simple customization or rebranding?

Brand change (also called rebranding) refers to the cosmetic adjustments made to the white label application to make it appear as though it was developed by your company. This process typically does not involve any modifications to the app’s core features or functionality, but focuses instead on the visual and branding aspects.

Key Characteristics:

- Logo Replacement: Changing the app’s logo to reflect your company’s brand.

- Color Scheme: Customizing the app’s design elements, like background colors, button styles, and fonts, to match your brand's style guide.

- Brand Identity: Incorporating your company’s name, slogans, or taglines within the app.

- Language changes: Implementation of new languages in the app

- Minor Content Updates: Updating in-app content (like text, images, or icons) to match your brand’s messaging, while the underlying functionality remains the same. That’s about changing the components itself - not the position of components on the screen.

Example: A new fintech provider purchases a white label delivery app. They change the app's color scheme to match their brand, update the logo, and add their business name throughout the app. However, the functionality (eKYC, payment system, transaction history, etc.) remains unchanged. This would be a brand change.

Summary:

- Custom Development: Involves altering the functionality of the app, adding or modifying features to meet specific business requirements.

- Brand Change: Involves changing the appearance of the app by applying your company's branding elements (logo, colors, etc.) without altering its core functionality.

Save time and reduce risks by choosing Verestro’s White Label solutions. With our ready-made, customizable apps, you can quickly launch your own branded product without the need for development or maintenance. Whether you need simple rebranding or more advanced custom features, Verestro’s proven solutions can help you scale faster. Contact Verestro today to explore how their expertise can elevate your business.

How does Verestro differ from standard software companies?

Verestro is a fintech-as-a- service provider - so we are not really interested in one-off projects - we are not a software house. We prefer to become your partner and help you thrive with our licensed technology, providing support and advice at every single step of your journey.

Verestro is a company focused on developing, maintaining and growing multiple fintech products. Let me give you some examples:

- If you are big manufacturer and you are interested in software to manage your production site - do not call us, it is not our domain of work, we do not want to focus time of our developers on such a project.

- If you are a global web provider and you are searching for new ways of building web services incl. Artificial Intelligence - do not call us, it is not what we are interested in.

- If you are a global technology company and you are interested in ERP software - do not call us, we are not interested in developing it for you.

- If you are a bank, and you are planning to launch a new credit scoring system - do not call us, we are not interested in it today (however, we are planning to work on credit processes as it is close to our fintech domain).

But if you are searching for various financial or payment solutions, especially if they require multiple integrations, are connected with all accounts, card issuing, card acquiring, contactless and eCom payments - call us. This is our domain where we are very strong. We can build very difficult use cases, we can connect card issuing with acquiring, we can play with technologies.

In other words we are focused on fintech products. We perform multiple certifications with VISA or Mastercard to be able to deliver these products globally in the most effective way. The best way to use our platform is actually to learn how our products work and try not to change too many things. We implement them in the best possible way, combining experience from various projects, geographies, and industries. If you use such products 'as-is', you will feel the most benefits as you will find out that implementing new payment innovations can be super quick (1-2 months) and very cost effective (10-20k EUR).

Test us, partner with us, play with fintech technology in a cost-effective way. Build a fintech innovation pipeline with us!

What is Verestro not doing?

Verestro is a Fintech-as-a-Service provider building a micro-service platform that enables our partners to launch multiple fintech innovations at very limited cost. Our core products are card issuing incl. global BIN sponsorship, tokenization through x-pays and other contactless payments, money transfer solutions, eCommerce payments, value added services incl. loyalty, virtual cards and expense management, white label apps and web front-end solutions.

In this article I would like to describe what Verestro does not do:

- Verestro is not a software outsourcing company focused on implementing IT projects outside of the fintech scope for particular customers. We do not do it and we do not want to do it.

- Verestro is not a software outsourcing company within the fintech scope if a particular development cannot be used as an additional benefit for the Verestro platform. We like technology projects that upgrade value of our multifunctional platform and deliver value for all our customers in the long run.

Let me give you more details on fintech products that we do not have live at the moment. But I can assure you that we will have them live soon:

- We do not have softPOS solutions enabling mobile phones becoming payment terminals. But we will be working on it.

- We do not have a full end-to-end mobile banking app. We have a white label app focused on fintech functionalities which - I think - can be treated as a mobile banking app, but we lack credit and investment related features. We can develop these functionalities for you if you are interested.

- On the acquiring side we do not have all local payment methods implemented. We are focused on global ways of payments like cards, Apple Pay, Google Pay. We will implement more local payment methods soon.

- Credit scoring - we do not have a credit scoring platform.

Our mission is: We are inspired by cutting-edge financial technologies and we make them affordable to everyone. If you are interested in going live with multiple payment innovations at an affordable price and extremely high speed, contact us!

Tokenize it!

Tokenization in Payments – How It Is Transforming Transactions

Tokenization has played a crucial role in contactless payments for years, evolving into a broad concept covering various technologies. Initially, it relied on hardware-based solutions like chips or SIM cards. Today, most systems use a device's standard processor, eliminating the need for dedicated hardware.

Every innovation in this field must comply with payment industry standards. Beyond implementation, security and formal approvals are equally critical. While Mastercard and Visa shape the market, tech giants like Apple and Google also drive payment evolution.

Regional Challenges and Service Development

Not all regions have equal access to payment services. Countries impose regulations requiring localized data processing. India mandates domestic storage of payment data, while Turkey requires accreditation from its central bank (CBRT) for external payment providers.

Apple Pay is widely available in regions like the United States and Europe, as well as in other major markets such as South Korea, Japan, and Australia. However, its availability is still limited in many parts of the world, meaning thet a significant number of iPhone users do not yet have access to contactless payments. By opening its ecosystem to external wallets, Apple creates new opportunities for banks and payment providers. Alternative mobile payment solutions on iPhones are now a reality.

Tokenization in E-Commerce and Mobile Applications

Tokenization extends beyond contactless payments, increasingly used in e-commerce and in-app transactions. Systems like DSRP (Digital Secure Remote Payment) and Click-to-Pay enhance convenience and simplify payments for merchants, particularly those avoiding complex PCI DSS procedures or adapting to regional regulations.

Wearable Payments – What’s Next?

Wearable payments are rapidly evolving. Smartwatch payments are common, while rings, glasses, and even clothing are gaining interest. The fintech industry will determine how quickly these innovations become mainstream. Soon, paying for coffee with a smart ring or VR glasses could be as easy as using a phone.

Tokenization not only simplifies transactions but also shapes the future of finance. The coming years promise even more advancements in this space.

What is an ACS in the 3DS Ecosystem?

In today's rapidly evolving digital landscape, online card-not-present (CNP) fraud remains a persistent challenge for financial institutions and merchants alike. 3D Secure (3DS), particularly its modern iteration, EMV 3-D Secure (3DS 2.x), stands as the industry's answer to this threat. This sophisticated security protocol introduces an essential layer of authentication for online credit and debit card transactions, aiming to drastically reduce fraud while simultaneously improving the customer experience.

ACS in the 3DS Ecosystem

The "3D" in 3DS refers to the three interconnected domains:

- Acquirer Domain: Encompassing the merchant and their acquiring bank, which processes card payments.

- Issuer Domain: Representing the cardholder's issuing bank, responsible for the card itself.

- Interoperability Domain: The underlying infrastructure and systems that facilitate seamless communication between the acquirer and issuer during a transaction.

At the heart of the Issuer Domain lies the Access Control Server (ACS). This is the technology that Verestro has now secured EMVCo approval for. The ACS is the brain behind the cardholder's authentication experience, operating in real-time to assess transaction risk and, when necessary, challenge the cardholder for verification.

Why Choose the Verestro ACS?

Building and certifying your own ACS can take over a year and cost upwards of €100,000. Verestro ACS provides a ready-to-use, fully certified solution that eliminates these barriers - offering rapid deployment, reduced costs, and full compliance.

Core functions of Verestro ACS

-

Verifying whether a card number is eligible for 3-D Secure authentication

-

Determining if the consumer's device type supports 3-D Secure

-

Authenticating the cardholder or confirming account information during transactions

Benefits of Verestro ACS

-

Enhanced Customer Experience: Offer a fast, intuitive, and secure checkout process - reducing cart abandonment and improving satisfaction.

-

Optimized Authentication Performance: Benefit from fast, reliable authentication flows that minimize delays and reduce failed transactions.

-

Device-Agnostic Compatibility: Ensure seamless operation across all channels - web, mobile browsers, and mobile apps.

-

Frictionless and Low-Friction Authentication: Support risk-based authentication and modern low-friction methods like biometrics, helping reduce step-up challenges.

-

Higher Approval Rates with Lower Fraud: Improve authorization rates by up while maintaining high security standards. Reduce fraud on 3DS-enabled transactions compared to non-3DS transactions.

-

Regulatory Compliance Made Easy: Stay fully aligned with evolving EMV® 3-D Secure standards and PSD2 SCA requirements - no additional development needed.

-

Faster Time-to-Market: Avoid long certification cycles and heavy infrastructure costs.

Key Features

-

EMVCo Certified

-

SaaS Model: Scalable, reliable, and maintenance-free

-

Simple API Integration: Fast time-to-market

-

Powerful Admin Panel

-

Browse and review authentication events in detail

-

Manage challenge screens and user flows via a flexible UI builder

-

Define custom rules with a highly configurable Rule Engine

-

Dashboard providing insights and key statistics at a glance

Authentication Flows

Frictionless Flow

- The cardholder is authenticated without any additional input, based on a real-time risk assessment using data such as transaction history, device information, and behavioral analytics.

- Best for low-risk transactions – no user disruption.

Challenge Flow

- The cardholder is required to complete a step-up authentication, such as entering a one-time passcode (OTP) or using biometrics.

- Used for higher-risk or non-recognized transactions.

3RI (Three Requestor Initiated)

- Authentication initiated by the merchant or payment service provider without the cardholder actively being involved (e.g., for subscriptions or card-on-file payments).

- Enables secure recurring or delayed transactions.

SPC (Secure Payment Confirmation)

A new flow supported by some browsers (notably in the EU), using WebAuthn and device biometrics to allow strong customer authentication in a streamlined, secure manner.

Combines strong security with an excellent user experience.

Authentication methods

- One-time passcode (OTP) sent via SMS

- Out-of-band verification through a mobile app

- Decoupled authentication

- Biometric authentication

- Other methods supported by EMV® 3-D Secure 2.3.1 and EMV® 3-D Secure 2.2.0

Device Channels

- App-based

- Browser-based

Regulatory Compliance

Verestro ACS is fully compliant with major standards and certifications, including:

- EMV® 3-D Secure 2.3.1

- EMV® 3-D Secure 2.2.0

- PCI-DSS

- PCI 3DS

Verestro is excited to continue empowering the future of payments by providing our clients with the cutting-edge technology - Access Control Server. This milestone reinforces Verestro's position as a trusted innovator, dedicated to making online transactions safer, smarter, and more seamless for everyone. If you are interested in our solution, don't hesitate to contact us.

Card Issuing & Bank Accounts

How does card issuing work? Check here.

Payment schemes

In this document we describe how payment schemes (Mastercard and VISA) work.

Payment card business is a large global market, which was developed in the USA in the first half of XX century and has grown globally. In this document we will describe the main business principles and in the next chapters we will go into more details. We will focus mainly on Mastercard and VISA operations, as these are the largest payment schemes in the world and the main partners we work with.

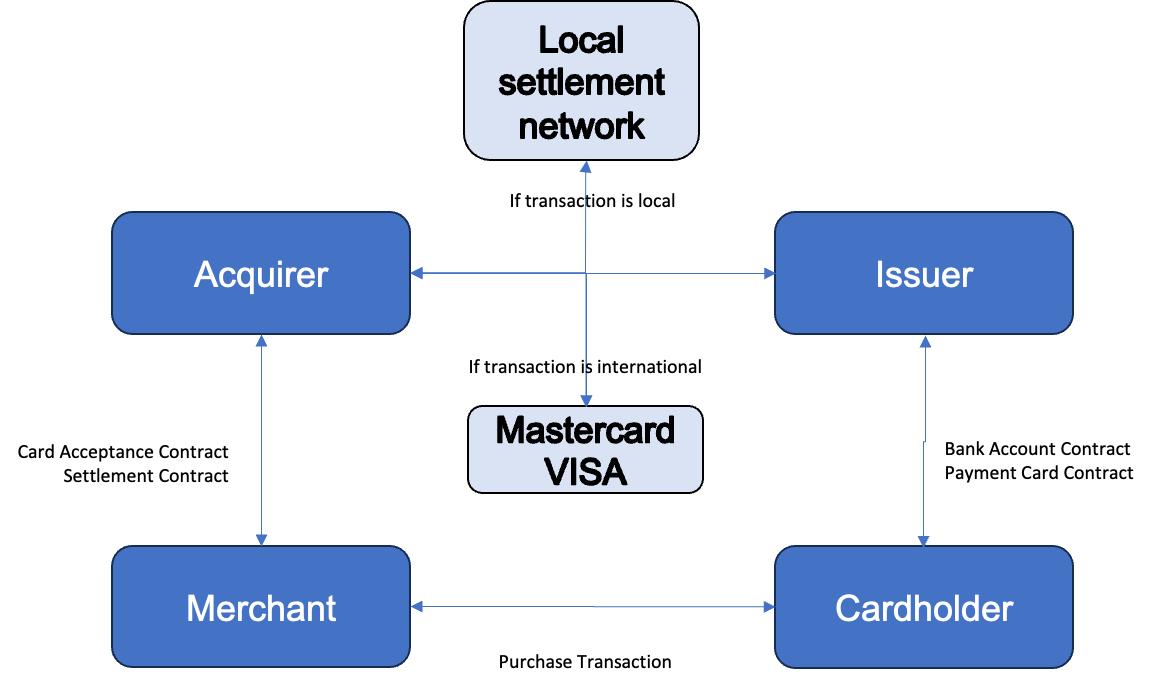

Four Party Model

Let's start with the general relationships between the parties. In the Mastercard and VISA 4-party model (which is actually 5-party model) there are the following players:

1. Cardholder - has a contract with Card Issuer, which is usually a bank, financial institution, payment institution, credit union, etc. Cardholder keeps a card in a plastic or virtual form that he/she gets from Issuer. Cardholder makes a purchase transaction at Merchant or sometimes withdraws money from an ATM. In the case of an ATM transaction, the ATM operator (usually a bank) acts as Merchant in a standard purchase transaction.

- Cardholder is happy because he/she does not need to carry cash all the time and has money all the time in their pocket or phone.

- Cardholder has to pay card fees to Issuer for getting a payment card.

2. Merchant - delivers goods to Cardholder, but does not receive cash immediately, but accepts the card transaction, which gives him/her almost 100% confidence that he/she will receive money in a few hours or days.

- Merchant is happy because he/she sold goods, usually having sold more than Cardholder could afford with cash. Imagine the situation where you have to pay cash all the time. Would you always carry enough cash with you? What if you want to buy something, but you do not have enough cash?

- Merchant has to pay the so called "Merchant Fees" to Acquirer for processing the transaction. Usually, Merchant Fees are between 0,5-3% depending on transaction value, country, merchant segment, type of card etc. Merchant fees cover most, if not all, of the transaction processing costs. They usually include all the fees charged by Acquirer, Issuer, Mastercard or VISA for the transaction.

3. Issuer - Issuer is usually a bank, credit union or any other payment institution that delivers payment cards to cardholders (consumers or businesses). Issuer signs contracts with cardholders. On the other side of business, Issuer has a franchising or licensing contract with VISA and Mastercard and connects to their network using Issuing Processors. Verestro and our partners plays the role of Issuer and Issuer Processor in our card issuing or BIN sponsorship projects. During the transaction process, Issuer usually gets authorization, clearing and settlement messages that result in transfer of money from a cardholder account to Acquirer so that Acquirer could settle the transaction with Merchant.

- Issuer is happy because they charge card fees to Cardholder (for example monthly per card) and get transaction fees called Interchange Fee from Acquirer. Interchange fee is a very important part of Merchant Fees. In the European Union for consumer cards it is usually in the value of 0,2-0,3%, but in many countries, especially for business and credit cards, it can amount to 1-2% of the transaction value.

- Issuer has to cover costs of card issuing, which include:

- Cost of payment scheme (Mastercard or VISA) incl. monthly connection, license, authorization, clearing and many many other fees. This is usually the main part of Issuer's costs.

- Cost of other processors incl. transaction authorisation, card maintenance, card tokenization, plastic card manufacturing, personalisation, delivery, etc.

- Regulatory costs incl. payment license operations, Anti-Money Laundering processes, etc.

- Various costs connected with maintaining a relationship with Cardholder incl. proper communications, SLAs, etc.

4. Acquirer - Acquirer is usually a bank or payment institution that signs contracts with merchants, settles payment transactions with merchants and has acquiring contracts with a payment scheme. Acquirer usually provides a payment terminal to merchant locations, and makes sure if it works and is ready for transactions.

- Acquirer is happy because they charge Merchant Fees that usually consist of transaction fees (0,5-3%), sometimes fixed fees per transaction (0,01-0,5 EUR) and monthly fees per terminal.

- Acquirer needs to cover various fees, including regulatory fees, payment scheme costs, cost of processors, terminal purchase and costs of operations.

5. Payment Scheme - Payment Scheme (i.e. Mastercard or VISA) are key for keeping the model running. They develop technical systems that issuers and acquirers are connected to, they process transactions, they develop the market. However, they are also the biggest beneficiaries of the market growth as every new transaction represents revenue for Mastercard and VISA.

Key Processes

There are several processes that take place during card and transaction processing, and here we will briefly describe the most important ones:

- Card issuing process - this process or set of processes consists of multiple actions that Card Issuer needs to perform to issue a payment card. They are the following:

- regulatory compliance - every card issuer in the world needs to comply with law, get license from a national bank or financial regulator, work according to their recommendations and rules,

- Mastercard integration and licensing - it consists of a formal process, providing necessary cash collaterals, doing technical integration, getting security certifications etc.,

- card creation process - after signing a contract by a user, Card Issuer needs to create a new card number (using BIN of the issuer - BIN = first 6 or 8 digits of card). When a card number (PAN = Primary Account Number) is created, the card can immediately work as a virtual card or can be sent for personalisation if it is a plastic card. Usually, after the user receives the card (virtual or plastic), the user starts the card activation process, sets the card PIN and can start using it.

- Transaction process - this process consists of several operations that result in transfer of money from Cardholder account to Merchant. They are the following:

- Authorization process is an action that ensures that Merchant can immediately get information if Cardholder has money on his/her card account and if this card is not stolen. The authorisation can happen online (a direct request to Issuer's system to check the balance and card status) or offline (in this case a chip on the card makes a decision if it can approve the transaction without asking Issuer's systems).

- Clearing process is an action of payment scheme during which clearing files are delivered by acquirers to payment scheme and payment scheme calculates how much money each Acquirer should receive from each Issuer in the world.

- Settlement process is a process of transferring money from issuers to acquirers and later to merchants so that finally Merchant receives the transaction amount, less Merchant Fees, on his/her bank account. Every Issuer and Acquirer has settlement bank accounts that are used for transferring money from or to. Payment Schemes operate those accounts using something like Direct Debit / Credit to transfer money between Settlement Accounts of various financial institutions.

- 3DS - sometimes additional authentication mechanisms are used to ensure that the person initiating the card transaction is the actual cardholder. In the case of eCommerce transactions this process is called 3DS. During an Internet transaction, the user's browser opens the bank's website, where the user can authenticate the transaction using one-time passwords or other forms of authentication developed by Issuer. After the 3DS authentication is verified, Acquirer receives a special cryptogram that is included in the authorization message and validated later by Issuer during the authorization process.

- Tokenization - tokenization is a process of exchanging a real card number into a token number (similar to a card number) to enable digital and contactless payments. Usually it is connected with transactions performed in cooperation with the so called X-Pays (i.e. Apple Pay, Google Pay, Fitbit Pay etc.). The process of tokenization requires an integration with Mastercard Digital Enablement System (MDES) or Visa Tokenization system (VTS) to enable tokenized payments.

- Refund and reversal - special type of transactions that enable reversing payment transaction either immediately (reversal) or later (refund). Once this process has been initiated, Cardholder can receive money back after successful authorisation.

- Chargeback - process of complaint management. It can be initiated by Issuer in case Cardholder informs Issuer that he/she did not do the transaction or did not authorize it, or goods were not delivered etc. The process is costly for Issuer and Acquirer but ensures security of the system for cardholders.

- Card-to-card transactions and payouts - the so called "payment" or "credit transactions". In a standard purchase transaction money is transferred from Cardholder to Merchant. In a card-to-card transaction or payout transactions, the user gets money on his/her card or on the account linked to the card.

There are other important processes associated with payment systems and card transaction processing, but let's stop here and take a short break to understand these critical processes.

Ranking of card issuing companies

How to choose a BIN sponsor and card issuing partner?

Choosing a BIN sponsor or card issuer is a difficult decision for many partners. Most of our partners do not come from the payment card business, so they learn by doing. In this chapter, we are going to describe the key decision factors of choosing a card issuer and make a simple ranking that we will be upgrading and updating in the coming months and years, as not all information is available to us immediately. On purpose, we will not compare other companies to us, it would not be fair to include Verestro - our goal is to educate in this article.

There are the following key decision factors in choosing a card issuing partner:

-

- Does the card issuer share 100% of interchange with me?

- What is the currency conversion rate that the card issuer shares with me?

- How can I impact and earn on ATM withdrawal fees?

- How can I impact and earn on various consumer fees?

- Can the partner help me with getting the Mastercard or VISA marketing and financial support in the short and long run?

2. COSTS - Obvious point.

-

- What are fixed and variable fees?

- What is the level of fees in case of low volumes and high volumes?

- Is there any opportunity to minimize costs as the business grows?

- Read this article for more info on standard card issuing costs: Card issuing - financial details

3. FUNCTIONALITY & SERVICE - a very important point. Critical in the long run.

-

- Does the partner have mandatory functionalities?

- Does the partner offer currencies that I need for my users?

- What are other products that can increase usability or profit that the partner offers?

- Maybe a loyalty program?

- Any insurance offers and additional benefits that could be sold to customers?

- Perhaps invoice scanning and expense management?

- Maybe white label solutions?

- Card reload mechanisms?

- Payouts to cards?

- etc.

- Does the partner offer quick access to a developer zone or a test environment?

- Does the partner make their APIs public?

3. SECURITY AND FINANCIAL STABILITY - a critical point. Maybe it should be the first one.

-

- Is the partner a small start-up, burning money or a payment institution generating profits? Can you imagine what would happen to your portfolio and users in case of bankruptcy or hostile takeover?

- Who are the shareholders of the partner? Are these venture funds or strategic, long term investors?

- Does the card issuer make their financial statements public?

- Does the partner offer support in solving PCI DSS issues (Payment Card Industry Data Security Standards)?

- Is the partner audited annually?

- Does the partner work with banks and other large financial institutions or focus only on small, high-risk startups?

- Is the partner a small start-up, burning money or a payment institution generating profits? Can you imagine what would happen to your portfolio and users in case of bankruptcy or hostile takeover?

Here's an initial comparison of the best known card issuers in the European Union (grades: low - high):

| Name | Country | Revenue Share | Costs | Functionality & Service | Security & Financial Stability |

| Treezor.com | France | Medium | High | Medium | Medium |

| Swan.io | Denmark | Medium | High | Medium | Medium |

| Dipocket.org | Lithuania | High | Medium | Low | Low |

| Solarisgroup.com | Germany | Medium | High | Medium | Medium |

| Wallester.com | Estonia | Medium | Medium | High | Medium |

| Stripe | USA | Low | High | High | High |

| Weavr.io | Malta | Medium | Medium | Low | Medium |

| Verestro | Poland | Make your own assessment | Make your own assessment | Make your own assessment | Make your own assessment |

Source: Financial Stability results based on 2022 or 2023 results available in Internet; all other data from publicly available sources. Please make your own assessment.

Card issuing - financial details

How can I earn from card issuing? This is a common question that is asked by our customers. Let me explain the key financial areas connected with this business.

Indirect revenue or cost savings

Usually, the main reason for issuing cards in different segments is indirect revenue or cost savings. The first question that you should ask yourself is connected with your use case. What can a payment card bring to my customers or my business? The answer to this question is different for various business segments and is the most important factor in defining a financial model for such an operation:

- If you are a bank, payment cards are obviously a core payment product that lets you earn from various transactions, currency conversions, ATM withdrawals and other fees.

- If you are a fintech wallet, it is obviously an important functionality because you compete with banks. It can increase your revenue streams from the same areas as above.

- If you are a crypto wallet, you want to offer to your customers a way to use digital assets at brick-and-mortar shops and in eCommerce.

- If you are an insurance company, you may want to send insurance in the form of a virtual card with a particular transaction and geographic limit so that your customer could immediately get necessary help.

- If you are an investment wallet, where users store value in the form of shares or bonds, you can offer payment cards to them so that they could pay using their shares at standard shops.

- If you are an eCommerce merchant or marketplace, you may be interested in using payment cards as a way to send back money to your users after their claim so that they could use this card for an eCommerce payment.

- If you are a small, medium or large corporation, you may want to distribute cards to your employees so that you limit costs of invoice processing and company invoicing.

- If you are an HR agency, you can use cards as a tool to pay salaries to your employees

- If you are a loyalty program owner, you may be interested in enabling users to use your points and make purchases at any location in the world.

- etc.

There are many use cases and this is the main value for you. You can charge additional fees for this new service offered to your users, or you can limit your operating costs thanks to card issuing. However, there are direct revenue streams and costs associated with issuing cards and I will describe them below:

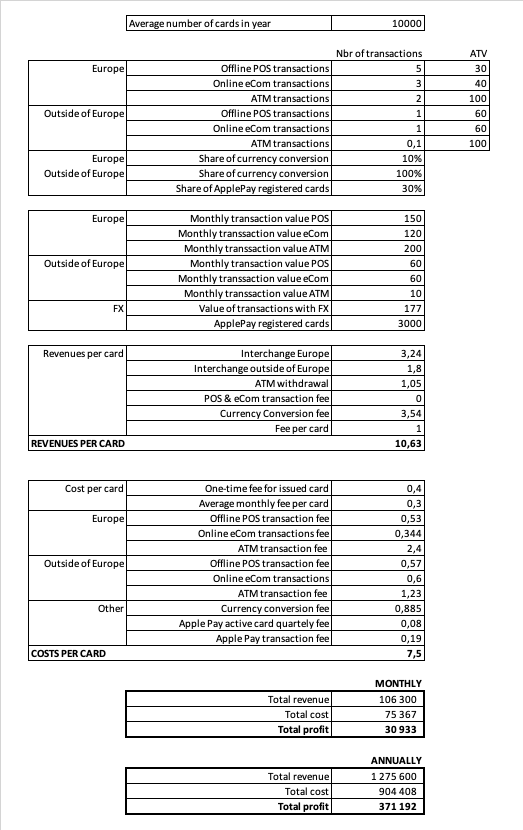

Direct revenues of card issuing

The following direct revenue is connected with card issuing and card transactions:

- Interchange Fee - when your user pays online or offline at any merchant, there is a fee called Interchange Fee that the issuer of cards receives for this transaction. The value of this fee depends on the country, transaction type, card product type, etc. In general, it is between 0,2% (for consumer debit cards issued in Europe) to 1-2% (for various types of cards for transactions done on other continents). Make sure you check with your card issuer or BIN sponsor how they share this fee with you - it is the most important revenue stream.

- Currency Conversion Fee - every card transaction done in another currency than currency of a card account results in currency conversion. This action usually enables charging fees. Typically, they are between 0,5% to 8% depending on card product, country, currency, etc.

- User fee - card issuers, banks, financial institutions usually charge various user fees for using their payment card. Examples of such fees are: one-time fee for issuing a card, monthly fee per card, annual fee per card.

- Transaction fees - depending on a card product and a type of transaction, card issuers charge users additional transaction fees. A very standard fee is an ATM withdrawal fee - it is almost always valid because there are direct costs of an ATM withdrawal called ATM Service Fee and these costs need to be covered. Sometimes card issuers charge POS or eCOM transaction fees - for example 0,1% fee for every transaction done with a card.

- Value added services - a card product enables you to charge additional services, i.e. insurances, VIP support, concierge etc. that increase your revenue streams.

Direct costs of card issuing

- One-time fee for card issuing - usually 0,1-1 EUR. This fee is charged at the moment of card issuing. This fee covers costs of payment processors, various costs of operations connected with issuing the first card.

- Monthly fee per card - usually you pay 0,1-1 EUR monthly per issued card. This covers both technical, regulatory and financial risk costs of card issuers.

- Transaction fees:

- per transaction (from 0,05-0,3 EUR) - depends on a type of transaction, region of transaction etc.

- per transaction value (from 0,01%-0,5%) - depends on a transaction value.

- ATM service fee - very specific fee which is part of a transaction fee in fact. For every ATM withdrawal, a card issuer needs to pay a fee which is transferred to an ATM operator. Usually, it is in the value of 0,5-3 EUR + 0-1% from the transaction value.

- 3DS operations fee - transactions in eCommerce require additional authentication. Such an operation usually results in an additional fee charged by a card issuer (0-0,04 EUR per transaction).

- Apple Pay fees - Apple charges additional fees for using Apple Wallet. Those fees are both per card quarterly and per transaction volume - different for POS transactions and inApp transactions. We are not allowed to disclose the level of these fees.

- Plastic card related fees - production, personalization and transport of plastic cards is a serious operation that involves various costs. Typically, between 2-5 EUR per card depending on customer location, type of card, etc.

These fees are usually charged by card issuers and BIN sponsors to their partners. They have to charge them because there are various costs that we need to cover (this issue also applies to Verestro and our BIN sponsors). The main card issuing costs are: