Article

You can find more knowledge about products on this site.

- Business Control for new or existing portfolios

- What employee benefits can be offered via the Verestro Business Control

- Card issuing - financial details

- Example of Profit & Loss calculation in card issuing

- Master balance and collateral in card issuing projects

- Financial Benefits and Costs of Card Issuing Models

Business Control for new or existing portfolios

One of our important products is Business Control. You can find more information about this solution under the following link - Business Control

Our customers are asking us from time to time if it is possible to use Business Control for the existing portfolio of customers and cards or if it is aimed for new customers. Let me clarify this topic in this article.

Business Control is a platform or set of functionalities targeted at business customers that should give them more control over spendings, company expenses, cost and invoice management and more. Verestro offers it to banks and fintechs as a technology platform or we also can deliver it directly to corporations in connection with our partnering payment institutions in various parts of the world.

It offers several important benefits for business customers:

- super easy issuing of virtual cards for various company expenses - imagine that your manager can issue a virtual card to you when you go to a conference in another country. Card will be valid for 2 weeks, will have various limits etc.

- invoice management - instead of collecting pictures or doing photos you just scan an invoice and it lands directly in finance or accounting department for approval and further processing

- employee benefits - you can use cards with multiply visuals to give Christmas gifts or Valentine Cards or Thank You Gifts to your employees

- all the money is held in one or a few payment accounts which means that you do not need to pre-paid every card. You keep money and deliver "limits" to your users. It is a very important benefit vs pre-paid cards.

Let's imagine that you already have a portfolio of business customers because you are a bank or fintech partner and you would like to offer such a platform to your customers. Quick answer is - of course it is possible to offer Business Control to your existing customers.

After some integration and implementation projects you will give your existing customers an opportunity to issue new virtual cards for their employees, manage invoices and expenses etc. However, take into account that if you would like to enable it for already issued cards, actually you are using just part of the functionalities. The card already exists, it is in hands of the user, so in fact it means that you will not issue a new card for this person but you can:

- manage limits of cards

- manage invoices

- have new interface for company / employee

- and additional possibility to issue new virtual cards for this company or business customer

Feel free to contact us and discuss details of such implementation.

Regards,

Krzysztof

What employee benefits can be offered via the Verestro Business Control

Our Business Control platform provides the opportunity to issue virtual cards and manage business expenses. But in fact it can be used in multiple ways for companies. Here are a few examples of such use cases:

- Business payment card - your employee going for a trip, conference, meeting with a customer can get a virtual payment card and use it for payments globally. Once the employee makes a transaction, he/she can scan an invoice and connect it with the transaction so that the finance team and accounting have an easier process of expense management. This is a usual use case.

- Salary card - you can send salaries to your employees worldwide by using Business Control. If you issue a card with a specific limit to your employee, the employee can start making purchases and use it as a normal card. Thanks to it you have an easy salary transfer mechanism to all employees globally.

- Lunch card - you can issue cards for your employees and offer them a virtual card as a lunch card to get some tax benefits (depending on the country). Thanks to Business Control you can limit the acceptance of these cards to dining so that employees could use the cards for meals.

- Gift cards, holiday gifts, Thank You Card - you can issue a virtual card via Business Control any time you want to reward a particular behaviour of your employees. It is a bonus for the employee. You can have a specific "bonus" or "holiday" related card visual, you can add a message to the employee so that he/she knows that this card is for the particular achievement.

- Limiting time for expense processing in the company - if you want to limit hours spent by your employees, administration, finance and accounting teams for expense processing, finding documents, connecting them with transactions, etc., you can use Business Control. We can integrate Business Control with your ERP system, we can transfer invoices and transaction data to your internal databases so that transactions can be processed automatically. Think how many hours you lose every month of such manual activities connected with expense management.

Please remember that we offer this product through partnering with payment or banking institutions. We can also offer it directly to companies in Europe. Contact us if you want to know more about this product.

Card issuing - financial details

How can I earn from card issuing? This is a common question that is asked by our customers. Let me explain the key financial areas connected with this business.

Indirect revenue or cost savings

Usually, the main reason for issuing cards in different segments is indirect revenue or cost savings. The first question that you should ask yourself is connected with your use case. What can a payment card bring to my customers or my business? The answer to this question is different for various business segments and is the most important factor in defining a financial model for such an operation:

- If you are a bank, payment cards are obviously a core payment product that lets you earn from various transactions, currency conversions, ATM withdrawals and other fees.

- If you are a fintech wallet, it is obviously an important functionality because you compete with banks. It can increase your revenue streams from the same areas as above.

- If you are a crypto wallet, you want to offer to your customers a way to use digital assets at brick-and-mortar shops and in eCommerce.

- If you are an insurance company, you may want to send insurance in the form of a virtual card with a particular transaction and geographic limit so that your customer could immediately get necessary help.

- If you are an investment wallet, where users store value in the form of shares or bonds, you can offer payment cards to them so that they could pay using their shares at standard shops.

- If you are an eCommerce merchant or marketplace, you may be interested in using payment cards as a way to send back money to your users after their claim so that they could use this card for an eCommerce payment.

- If you are a small, medium or large corporation, you may want to distribute cards to your employees so that you limit costs of invoice processing and company invoicing.

- If you are an HR agency, you can use cards as a tool to pay salaries to your employees

- If you are a loyalty program owner, you may be interested in enabling users to use your points and make purchases at any location in the world.

- etc.

There are many use cases and this is the main value for you. You can charge additional fees for this new service offered to your users, or you can limit your operating costs thanks to card issuing. However, there are direct revenue streams and costs associated with issuing cards and I will describe them below:

Direct revenues of card issuing

The following direct revenue is connected with card issuing and card transactions:

- Interchange Fee - when your user pays online or offline at any merchant, there is a fee called Interchange Fee that the issuer of cards receives for this transaction. The value of this fee depends on the country, transaction type, card product type, etc. In general, it is between 0,2% (for consumer debit cards issued in Europe) to 1-2% (for various types of cards for transactions done on other continents). Make sure you check with your card issuer or BIN sponsor how they share this fee with you - it is the most important revenue stream.

- Currency Conversion Fee - every card transaction done in another currency than currency of a card account results in currency conversion. This action usually enables charging fees. Typically, they are between 0,5% to 8% depending on card product, country, currency, etc.

- User fee - card issuers, banks, financial institutions usually charge various user fees for using their payment card. Examples of such fees are: one-time fee for issuing a card, monthly fee per card, annual fee per card.

- Transaction fees - depending on a card product and a type of transaction, card issuers charge users additional transaction fees. A very standard fee is an ATM withdrawal fee - it is almost always valid because there are direct costs of an ATM withdrawal called ATM Service Fee and these costs need to be covered. Sometimes card issuers charge POS or eCOM transaction fees - for example 0,1% fee for every transaction done with a card.

- Value added services - a card product enables you to charge additional services, i.e. insurances, VIP support, concierge etc. that increase your revenue streams.

Direct costs of card issuing

- One-time fee for card issuing - usually 0,1-1 EUR. This fee is charged at the moment of card issuing. This fee covers costs of payment processors, various costs of operations connected with issuing the first card.

- Monthly fee per card - usually you pay 0,1-1 EUR monthly per issued card. This covers both technical, regulatory and financial risk costs of card issuers.

- Transaction fees:

- per transaction (from 0,05-0,3 EUR) - depends on a type of transaction, region of transaction etc.

- per transaction value (from 0,01%-0,5%) - depends on a transaction value.

- ATM service fee - very specific fee which is part of a transaction fee in fact. For every ATM withdrawal, a card issuer needs to pay a fee which is transferred to an ATM operator. Usually, it is in the value of 0,5-3 EUR + 0-1% from the transaction value.

- 3DS operations fee - transactions in eCommerce require additional authentication. Such an operation usually results in an additional fee charged by a card issuer (0-0,04 EUR per transaction).

- Apple Pay fees - Apple charges additional fees for using Apple Wallet. Those fees are both per card quarterly and per transaction volume - different for POS transactions and inApp transactions. We are not allowed to disclose the level of these fees.

- Plastic card related fees - production, personalization and transport of plastic cards is a serious operation that involves various costs. Typically, between 2-5 EUR per card depending on customer location, type of card, etc.

These fees are usually charged by card issuers and BIN sponsors to their partners. They have to charge them because there are various costs that we need to cover (this issue also applies to Verestro and our BIN sponsors). The main card issuing costs are:

- Payment scheme fees - Mastercard, VISA or any other payment organization charge a lot of various fees for connecting with them and using their licenses and technology. This is one of the biggest components of costs for card issuers.

- Payment processors - this is our (Verestro's) role. To issue cards, you usually need to hire external, certified payment processors. They charge a lot of fees for using their technology. Examples of such processors are : Verestro :) , Paymentology, Fiserv, First Data, Marqueta etc.

- Card manufacturers and personalisation centers - if you issue or sell plastic cards, you need to produce and personalize these cards. Companies like Austriacard, Thales, Idemia charge fees for such operations.

- Regulatory compliance costs - to become a card issuer in any country, you need to have a payment license, get certification, fulfill necessary roles that are not present in another business. This is a serious cost for card issuers.

- Security costs - to work with payment cards and process them, you need to fulfill various security requirements. The most important ones are summarized in the Payment Card Industry Data Security Standards. They include not only internal actions but also annual and quarterly audits that you need to perform to be compliant and offer secure operations.

There are other possible revenue streams and costs connected with card issuing, but the ones described above are the most important ones.

Thank you for reading.

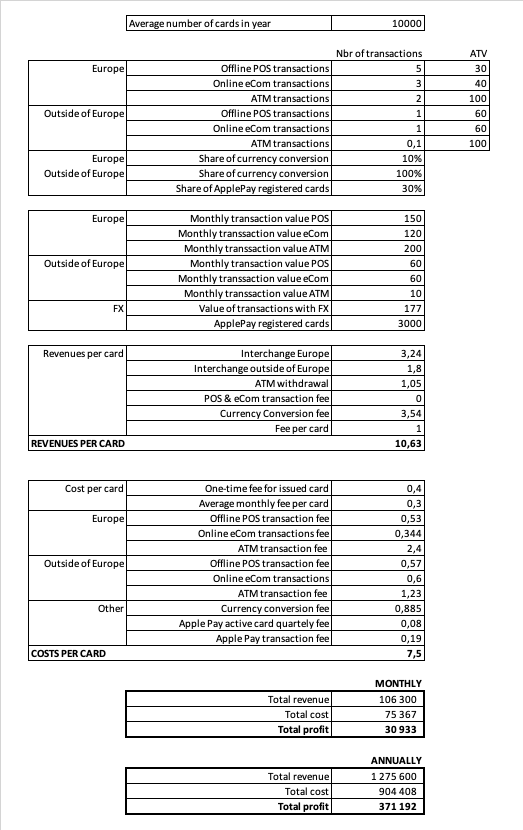

Example of Profit & Loss calculation in card issuing

Calculating profits and losses in card issuing is not easy, especially when various card issuers offer different fee and revenue models. Below I would like to show a few examples.

Let's imagine we are a fintech wallet with 10.000 users and we would like to issue cards for these users. The first step we need to take is to try to forecast key parameters of product, transaction, revenue and cost assumptions:

- Product

- Product - Debit Business Mastercard card

- Settlement currency - EUR

- Transactions

- Average number of cards in a year - 10.000

- Offline POS transactions in Europe: Number of transactions per month - 5 ; Average Transaction Value (ATV) - 30 EUR

- Online eCom transactions in Europe: Number of transactions per month - 3 ; ATV - 40 EUR

- ATM transactions in Europe: Number of transactions per month - 2 ; ATV - 100 EUR

- Share of currency conversion transactions in Europe - 10% (transactions done in Polish zloty, Czech koruna, Romanian Lei, Swedish krona etc.

- Offline POS transactions outside of Europe: Number of transactions per month - 1 ; Average Transaction Value (ATV) - 60 EUR

- Online eCom transactions outside of Europe: Number of transactions per month - 1 ; ATV - 60 EUR

- ATM transactions outside of Europe: Number of transactions per month - 0,1 ; ATV - 100 EUR

- Share of currency conversion transactions outside of Europe - 100% (transactions done in Polish zloty, Czech koruna, Romanian lei, Swedish krona etc.

- Share of registered ApplePay cards - 30%

- Share of ApplePay transactions - 20% for online and 90% for offline contactless

- Revenue

- Interchange fee for business cards (fee from POS and eCommerce transactions; we assume 100% of interchange stays with partner)

- in Europe - 1.2%

- outside Europe - 1.5%

- ATM withdrawal fee - 0.5%

- POS and eCommerce transaction fee - 0%

- Currency conversion fee - 2%

- Monthly fee per card - 1 EUR

- Interchange fee for business cards (fee from POS and eCommerce transactions; we assume 100% of interchange stays with partner)

- Costs

- One-time fee for an issued card - 0,4 EUR

- Average monthly fee per card - 0,3 EUR

- Fee for offline POS transactions in Europe - 0,10 EUR + 0,1%

- Fee for online eCom transactions in Europe - 0,10 EUR + 0,11%

- Fee for ATM transactions in Europe - 0,9 EUR + 0,3%

- Fee for offline POS transactions outside of Europe - 0,3 EUR + 0,45%

- Fee for online eCom transactions outside of Europe - 0,3 EUR + 0,5%

- Fee for ATM transactions outside of Europe - 0,3 EUR + 1.2%

- Currency conversion fee - 0,5%

- Apple Pay active card quarterly fee - 0,25 EUR

Let's do quick calculations.

Please treat it as example and make your own calculation. There will be many dependencies connected with segment, type of portfolio, detailed pricing, volume estimations etc.

Taking into account the above assumptions, you could earn 30.933 EUR monthly and 371.192 EUR annually on such a portfolio. Seems high? Interested what cost of investment is needed? Contact us.

Thanks for reading.

PS. If you are interested in receiving an Excel file related to these calculations, let us know at sales@verestro.com.

Master balance and collateral in card issuing projects

During the implementation of card issuing projects with Verestro and our partner payment institutions, we receive questions about liquidity management and collateral in card issuing projects. Let me summarize and explain the key dependencies.

There are two important points that need to be taken into account:

1. Collateral - this is a dedicated amount of money and account which needs to be transferred by our partner to our account to cover costs of payment risks and collateral that we need to pay to Mastercard or VISA. Usually it is between 3-5 days of transaction volume. The collateral is non-refundable until the end of the project and may grow in time together with the volume of transactions. If we do not take collateral, there is a risk that in case of growth, we will have to block the partners' transactions because we will not have enough liquidity at Mastercard or VISA accounts.

2. Master balance - it is an account (in other words cash balance) dedicated to our card issuing partners where our partner stores his own money which covers fees paid to our card issuing partners and/or transaction settlement in case of working with external balance API. There are two possible situations that affect the amount of the master balance:

-

- Scenario 1 - In case External balance API is used which means that partner keeps information about user balance and every transaction authorisation is routed to partner for approval. In such a case we have to keep the Master balance of the partner up to the amount of transactions. Every transaction authorisation is verified by the partner but also on our Master balance account. A day later we have to settle money for this transaction with Mastercard so we must have enough cash on Master balance to cover this transaction amount. Every day or any time our partner transfers additional money to the Master balance to make sure that there is enough liquidity to cover costs of transactions of their users. This means that the amount on the Master balance is high enough to cover transactions of users during a day, week etc.

- Scenario 2 - In case internal balances are used, we have a situation where all users' money are kept at our payment institution. It means that the partner does not need to provide additional funds to cover transaction volume. In such a case the partner needs to transfer just an adequate amount to cover the amount of transaction and card fees to be paid for card issuing activities.

In all card issuing projects both collateral and masterbalance exist so please make sure you are aware of differences between those two definitions.

Thanks for reading.

Financial Benefits and Costs of Card Issuing Models

In this article we will focus on the three main business models of cooperation in card issuing programs: co-brand, affiliate license and principal membership. We will explain the key advantages and disadvantages of each model.

Co-brand

The easiest model of all. Our BIN sponsors create a new card visual for you, we dedicate a BIN range, and you can issue cards. All settlements are done between the partner and the BIN sponsor. There is no contractual direct relation between the partner and the payment scheme (VISA or Mastercard). The partner usually receives 90-100% of interchange fee and vast majority of currency conversion revenues. In this case the partner needs to provide a collateral to the BIN sponsor – usually 4-5 days of the forecasted turnover. This model is the most cost effective one – no big operations on the partner side, no licensing costs, no difficult implementations. You can go live with your program within 1-2 months for around 10-20k EUR.

The main disadvantage is that the BIN sponsor will have to have contract with partners’ users as formally they open a payment account and get a payment card from the BIN sponsor.

Affiliate license

An affiliate license is the first step to your own license. The partner wants to have a direct relationship with the payment scheme and the partner must have a payment license in the country (like EMI). The partner wants to see a detailed cost split and cost of payment organizations. Our BIN sponsor will register the partner at Mastercard as an affiliate licensee. Mastercard will do a verification of the partner and will approve the application – additional 3-4 months will be needed for the project. In this model, the Partner will usually get a detailed split of Mastercard fees and 100% of interchange. For settlements and fees the partner will be settling with the BIN sponsor / our payment institution. The partner will have to pay an additional collateral and additional Mastercard fees (around 2-4k EUR per month). A big advantage is that there will be no additional contract with users – just the partner contract with users. A slight advantage and disadvantage is that the partner can usually see all info about the settlements with Mastercard for his/her cards.

The main disadvantages are time (extra 3-4 months) and additional costs.

Principal license

The most sophisticated and most difficult model of cooperation with a payment scheme. The partner must be a payment institution in the country working under the regulatory approval. There will be no BIN sponsor involved in such a project as the partner will have their own license. In this case Verestro will act as a card issuing processor supporting the partner in integrations and operations with Mastercard or VISA. The partner will have to pay collateral to Mastercard and VISA (usually from zero at the beginning to millions of EUR if you issued 100.000 cards), so the liquidity will be needed for operations. The partner will settle transactions directly with the payment scheme through settlement banks where accounts will have to be opened. The partner will get 100% of interchange fee and all currency conversion revenues. The partner will have to take care of plastic card operations, chargebacks, settlements, liquidity etc. You will need 5-10 people minimum to perform those operations. The users will have a contract with the partner only.

The main disadvantage is cost (additional 100-150k EUR to be paid to payment schemes) and time of implementation (5-10 months).

In summary:

• Co-brand – use it when you want to go live quickly and pay little; use it when you are not sure if you issue >200.000 cards

• Affiliate – use it in specific cases only if you must have a license for whatever reason and you want to avoid that your customers sign a contract with an external institution

• Principal – use it when you are big enough, you are sure you can issue >200.000 cards, make sure you have enough money (>1mln EUR) for liquidity and cost of operations

Sometimes, the best model is to start with a co-brand license and migrate to a principal license once you grow. We can help you with this scenario, so you won't have to make those difficult decisions. The migration process could be very smooth in such cases.

Krzysztof Drzyzga